Key points: The Federal Reserve cut rates by 25 basis points for the third consecutive time, as the market expected, but this is the first time since 2019 that there were three votes against the interest rate decision.

Milan, who was 'appointed' by Trump, continues to advocate for a 50 basis point rate cut, while two regional Fed chairs and four non-voting members support maintaining the status quo, effectively resulting in seven opposing the decision. Reportedly, this disagreement is the largest in 37 years.

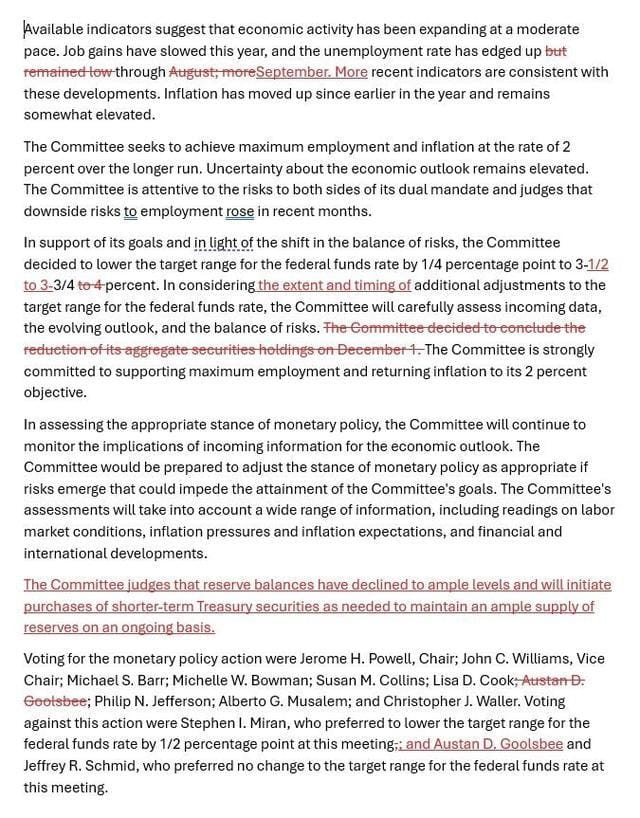

The meeting statement reiterates that inflation remains slightly elevated, and the risk of employment declining has increased in recent months, removing the statement that the unemployment rate 'remains low' and indicating a slight increase as of September.

The statement added considerations for the 'magnitude and timing' of further rate cuts, which is seen as implying that the threshold for rate cuts is higher.

The statement said that reserves have dropped to sufficient levels, and to maintain adequate reserves, short-term bonds will start to be purchased this Friday. The New York Fed plans to buy $40 billion in short-term bonds over the next 30 days, expecting high levels of bond purchases in the first quarter of next year.

The median expected value of interest rates remains unchanged from the last time, indicating that a rate cut is expected once in the next two years, with the dot plot's interest rate forecast for next year changing to a more dovish stance, with one less person expected to vote for no rate cuts, totaling seven.

The economic outlook for this year and the next three years has been raised, while the inflation and unemployment rate expectations for this year and next have been slightly lowered.

The 'new Fed press agency' suggests that the Fed hints it may not cut rates again for the time being because there is a 'rare' disagreement over which is more concerning: inflation or employment.

As expected by the market, the Federal Reserve again cut rates at a regular pace, but revealed the largest internal disagreement among voters in six years, suggesting that actions will be slowed next year and may not take action in the near term. The Fed also initiated reserve management as Wall Street anticipated, deciding to buy short-term government bonds at the end of the year to respond to pressure in the money market.

On December 10, Wednesday, Eastern Time, the Federal Reserve announced after the FOMC meeting that the target range for the federal funds rate was lowered from 3.75% to 4.00% to 3.50% to 3.75%.

Thus, the Federal Reserve has cut rates for the third consecutive FOMC meeting, each time by 25 basis points, with a total cut of 75 basis points this year, and a total cut of 175 basis points in this round of easing since last September.

The dot plot released after the meeting shows that the interest rate path forecast of the Federal Reserve's decision-making body remains consistent with the dot plot released three months ago, still expecting one 25 basis point rate cut next year. This indicates that next year's rate cut actions will be significantly slower than this year.

This rate cut and the hint of slowing actions next year were almost entirely anticipated by the market. By the close on Tuesday, CME tools indicated that the futures market expected a nearly 88% probability of a 25 basis point rate cut this week.

The probability of at least a 25 basis point rate cut next year in June will only reach 71%. The probabilities of such cuts during the meetings in January, March, and April have not exceeded 50%.

The predictions reflected by the aforementioned CME tool can be summarized by the recently discussed term 'hawkish rate cut.' This refers to the Fed cutting rates this time, while simultaneously hinting at a possible pause in actions thereafter, indicating no further rate cuts in the near term.

Nick Timiraos, a veteran Fed reporter known as the 'new Fed press agency,' bluntly stated in a post after the Fed meeting that the Fed 'hinted that it may not cut rates again for the time being' due to a 'rare' disagreement over which is more concerning: inflation or the labor market.

Timiraos pointed out that three officials disagreed with the 25 basis point rate cut at this meeting, with stagnation in the downward trend of inflation and a cooling labor market leading to this meeting being one of the largest disagreements in recent years.

Furthermore, it was noted that the dot plot released shows that, including two voting FOMC members, a total of six expect no rate cut in December, in other words, a total of seven oppose this 25 basis point rate cut, marking the largest disagreement in 37 years.

This is the first time since 2019 that there were three votes against the interest rate decision.

Compared to the last meeting's decision at the end of October, the biggest difference in this meeting's statement is that among the 12 FOMC voting members, a total of three voted against the 25 basis point rate cut, one more opposing vote than at the end of October. This is the first time since 2019 that the Federal Reserve's interest rate decision faced opposition from three voting members.

The statement shows that, including Federal Reserve Chair Powell and the previously publicly threatened to be fired Fed Governor Cook, a total of nine FOMC members support continuing to cut rates by 25 basis points.

The three dissenting votes were cast by Stephen Miran, the Fed governor 'appointed' by Trump, Austan Goolsbee, the president of the Chicago Fed, and Jeffrey Schmid, the president of the Kansas City Fed.

Among them, Milan has consistently sought a 50 basis point rate cut, as he did in the first two meetings he attended since taking office. Schmid, like at the last meeting, opposed because he supported keeping rates unchanged. Goolsbee, who supported a 25 basis point cut last time, has changed his position this time and stands with Schmid.

This year, there have been four FOMC meeting decisions with opposing votes. There were two opposing votes in July and the last meeting, while in September, only one dissent from Milan.

These voting disagreements reflect that, in the context of government shutdowns leading to some official data not being disclosed timely or even permanently missing, Federal Reserve decision-makers do not have a unified risk assessment regarding inflation and employment.

Those opposing the rate cut are mainly concerned about the stagnation of the downward trend in inflation, while those supporting the cut believe that action should continue to avoid accelerating job losses and worsening labor market conditions.

Newly added considerations for further rate cuts 'magnitude and timing.'

Another major change in this meeting's statement compared to the last is reflected in the interest rate guidance. Although this time the decision was to cut rates, the statement no longer vaguely states that when considering further rate cuts, the FOMC will assess future data, the continuously changing outlook, and risk balance, but rather more clearly considers the 'magnitude and timing' of rate cuts. The statement changed to:

When considering the magnitude and timing of further adjustments to the federal funds rate target range, the FOMC will carefully assess the latest data, the continuously changing economic outlook, and the risk balance.

Following the above statement, the Fed statement continues to reiterate its firm commitment to support full employment and to let the inflation rate fall to the Fed's target level of 2%.

This aligns with the adjustments previously anticipated by Wall Street. They expect the statement to return to the style of a year ago, reusing phrases like 'magnitude and timing of further adjustments.' Goldman Sachs believes that such adjustments reflect that 'the threshold for any further rate cuts will be higher.'

Removed the statement that the unemployment rate 'remains low,' indicating a slight increase as of September.

Other economic evaluations in the statement mostly use the wording from the last statement. To reflect the impact of insufficient official data, it reiterates that 'available indicators show that the pace of economic activity expansion has moderated.'

The statement reiterated that employment growth has slowed this year, with slight adjustments to the description of the unemployment rate. The last statement said, 'the unemployment rate has risen slightly, but remains low as of August,' this time it changed to 'the unemployment rate has risen slightly as of September,' removing 'remains low.'

Following these remarks, the statement indicated that more recent indicators are consistent with these trends, reiterating that inflation rates have risen slightly since the beginning of the year and remain somewhat elevated.

Like last time, this statement also notes that the FOMC 'is focused on the risks facing its dual mandate and assesses that the risk of employment decline has increased in recent months.'

Plans to buy $40 billion in short-term bonds over the next 30 days, expecting high levels of bond purchases in the first quarter of next year.

Another important change compared to the last meeting's statement is that this time a new paragraph was added, specifically pointing out the need to purchase short-term bonds to maintain a sufficient supply of reserves within the banking system. The statement reads:

The committee believes that the reserve balances have dropped to sufficient levels and will begin purchasing short-term government bonds as needed to continuously maintain adequate reserves.

This is tantamount to announcing the start of so-called reserve management to rebuild liquidity buffers in the money market. Since market chaos often occurs at the end of the year, banks typically reduce their activities in the repurchase market at year-end to support their balance sheets in response to regulatory and tax settlements.

The following red text shows the deletions and additions in this decision statement compared to the last one.

The New York Fed, responsible for open market operations, issued a notice this Wednesday, stating that it plans to buy $40 billion in short-term government bonds over the next 30 days.

The New York Fed, responsible for open market operations, issued a notice this Wednesday, stating that it plans to buy $40 billion in short-term government bonds over the next 30 days.

The New York Fed announced that it received instructions from the FOMC to increase the securities holdings in the System Open Market Account (SOMA) by maintaining adequate reserves through purchasing short-term government bonds in the secondary market and buying government bonds with a remaining duration of up to three years when necessary.

The scale of these reserve management purchases (RMP) will be adjusted based on expectations of the demand for Federal Reserve liabilities and seasonal fluctuations, such as tax day impacts.

The announcement states:

The monthly RMP amount will be announced around the ninth working day of each month, along with a provisional purchase plan for the next 30 days. The trading desk plans to announce the first plan on December 11, 2025, at which time the total amount of RMP short-term government bonds will be approximately $40 billion, with purchases starting on December 12, 2025.

The trading desk expects that to offset the significant increase in non-reserve liabilities expected in April (next year), RMP purchases will remain at a high level in the coming months.

Subsequently, the total purchase pace may significantly slow down based on expected seasonal changes in Federal Reserve liabilities. The purchase amount will be appropriately adjusted based on the outlook for reserve supply and market conditions.

The dot plot shows that there were seven dissenters in this decision, and the interest rate forecast for next year has changed to a more dovish stance compared to the last meeting.

The median value of interest rate forecasts released by Federal Reserve officials after this Wednesday's meeting shows that the expectations of Federal Reserve officials this time are exactly the same as the last predictions released in September. The specific median values of the predictions are as follows:

The federal funds rate at the end of 2026 is expected to be 3.4%, the federal funds rate at the end of 2027 is expected to be 3.1%, and the federal funds rate at the end of 2028 is expected to be 3.1%, with the longer-term federal funds rate remaining at 3.0%, all unchanged from September's expectations.

Based on the median value of the aforementioned interest rates, like last time, Federal Reserve officials currently also expect that after cutting rates three times this year, there will be approximately one 25 basis point rate cut each next year and the year after.

Thank you for watching. I am Xiao Fei, and I am happy to meet everyone. I focus on Ethereum contract spot ambush. The team still has positions, so get in quickly and become the dealer, and also become a winner. #加密市场反弹 $ETH$BTC