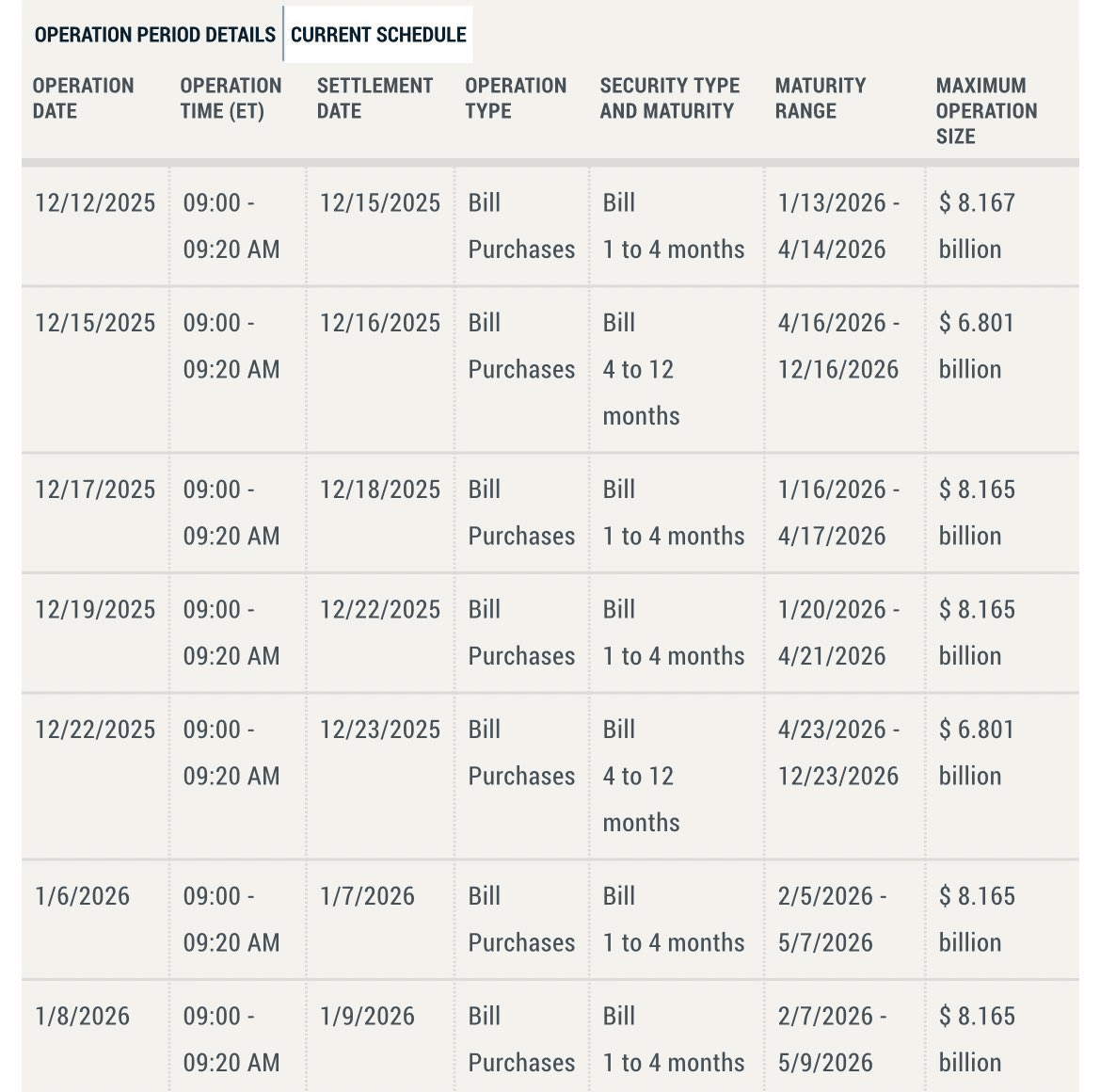

On December 12, the Federal Reserve officially launched a monthly purchase plan for $40 billion in short-term Treasury bills, marking a further increase in its liquidity support through monetary policy operations to alleviate the tight reserve situation in the banking system and stabilize year-end funding market fluctuations. Although this technical easing measure differs from traditional quantitative easing, it has significantly changed market liquidity expectations, leading to short-term adjustments across various asset classes.

This bond purchase action is not coincidental but rather a targeted response by the Federal Reserve to the residual effects of prior balance sheet reduction. As the previous balance sheet reduction progressed, reserves in the banking system gradually declined from the 'ample' range, short-term interest rate fluctuations intensified, and overnight repo rates repeatedly approached the upper limit of the policy rate, with the risk of a year-end funding crunch continuously rising. Against this backdrop, the Federal Reserve not only launched a $40 billion Treasury bill purchase plan each month but will also reinvest maturing agency debt, with an additional purchase of about $14.4 billion in Treasury bills in December alone, providing dual support to 'water' the market.

The effects of liquidity injection have begun to show. After the announcement, trading volume in short-term interest rate futures surged, the two-year swap spread widened to a new high since April, and the short-term borrowing costs fell in response, significantly easing market concerns about financing pressure. Wall Street investment banks quickly raised their expectations, with Barclays predicting that the total amount of Fed purchases could approach $525 billion by 2026, and JPMorgan also forecasting that the total purchases for the year will reach $490 billion, which means the Fed will become the dominant buyer in the short-term Treasury market.

However, the market is not entirely optimistic. Some institutions pointed out that this round of bond purchases, while effective in supporting liquidity, is not a 'panacea' for year-end funding pressures. The scale of purchases in December is still unlikely to fully cover the year-end overnight funding demand, compounded by the fact that banks typically shrink their balance sheets and limit repurchase activities at year-end, which may still lead to volatility in the short-term funding market. Additionally, the Fed's signal of 'concurrent easing actions and tightening guidance' has complicated market expectations, and the anticipation of higher forward rates continues to suppress the upside potential for risk assets to some extent.

Overall, the Fed's bond purchases have initiated a new phase of liquidity supplementation, which will significantly improve the tense funding situation in the short term, but the long-term impact will still depend on adjustments in the pace of bond purchases and changes in policy guidance. Against the backdrop of the Treasury's increased debt issuance efforts, this operation has become a key variable in the balance of supply and demand for U.S. Treasuries and the trend of short-term interest rates in 2026, and the market will continue to focus on its actual effects and policy direction.$BTC $ETH #美联储降息 #加密市场反弹 #美联储FOMC会议 #美SEC推动加密创新监管 #加密市场观察