You know, one of the main paradoxes of DeFi that has long annoyed me is the necessity of having huge amounts in collateral to obtain relatively small liquidity. Imagine: you have cryptocurrency worth $10,000, you collateralize it, and you only get a loan of $3,000-4,000. The rest of the money just hangs as dead weight, not working, not generating income. It's like buying a house for a million to rent out one room for pennies. Economically absurd, but that's how most lending protocols operated before solutions like @falcon_finance came along.

Let's figure out what capital efficiency actually means. It is a measure of how productively your capital is used. If you invested $10,000 and got the ability to operate only $4,000, your efficiency is 40%. And what about the remaining 60%? They are frozen, as if you put the money under the mattress "just in case." And yes, I understand the logic — it's protection against volatility, insurance against liquidation. But surely there must be a better way?

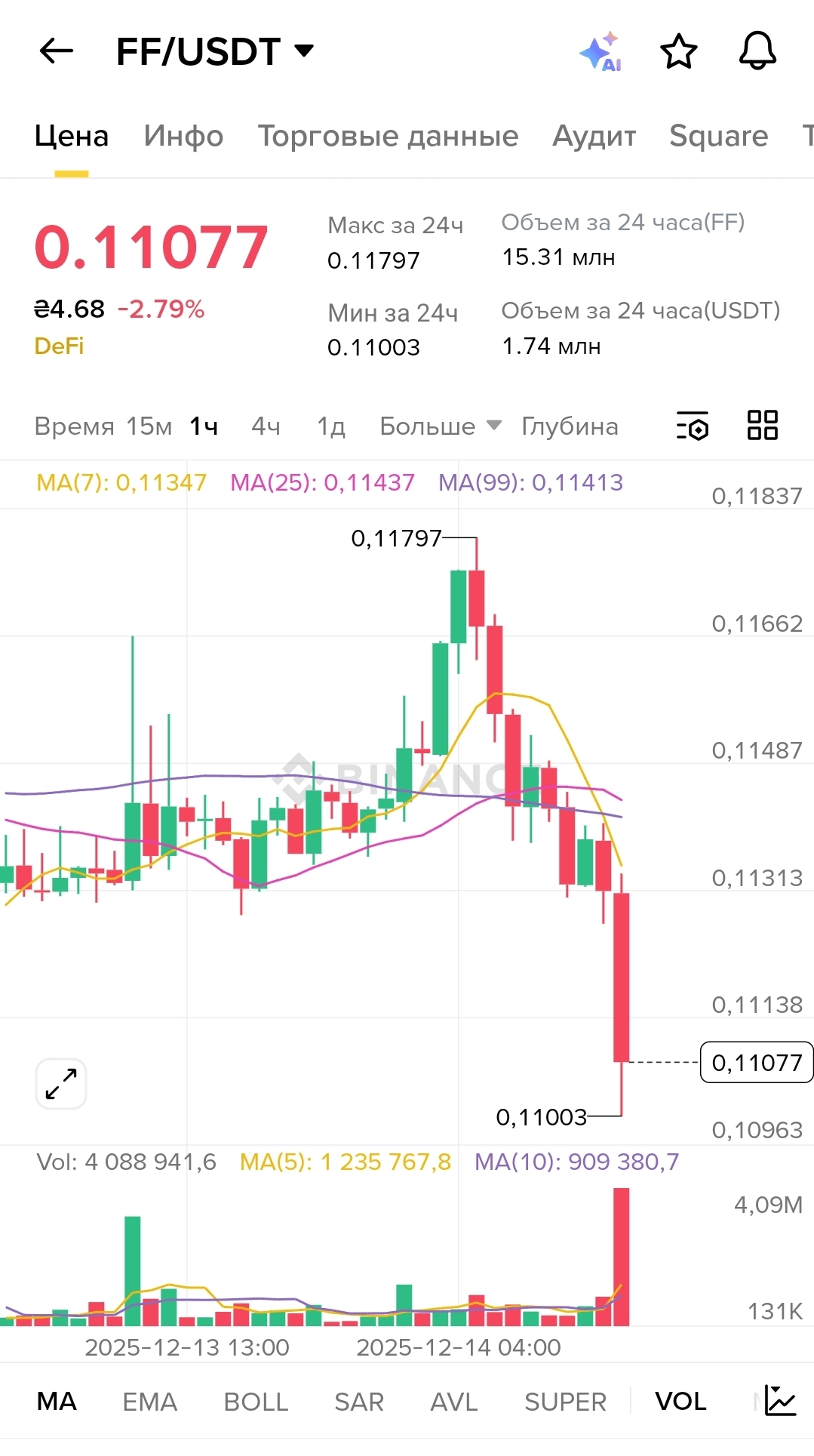

I look at the current chart of $FF and see a clear example of why capital efficiency is so important. The price is now 0.11077 USDT, down 2.79% in a day. Over the last 24 hours, the token fluctuated from a low of 0.11003 to a high of 0.11797 — a range of 7.2%. It is precisely because of such volatility that most protocols require excessive collateral of 150-200%. But #FalconFinance approaches this problem differently.

The traditional model works like this: the higher the volatility of the asset, the greater the safety margin must be, and the lower the capital utilization ratio. This makes sense, but it also means your money is working at half power. And if we look at the trading volumes $FF — 15.31 million per day for the token and 1.74 million USDT — it becomes clear that the asset is liquid, traded actively, which means there is an opportunity to manage risks more flexibly without the need to maintain huge reserves.

Do you know what impressed me about @falcon_finance's approach? The universal collateral infrastructure allows the use of different types of assets — from volatile tokens to stable tokenized real-world assets. And this is where the magic begins. If you diversify your collateral by combining high-risk and low-risk assets, the overall risk profile of the portfolio becomes more balanced. And this means that you can increase the capital utilization ratio without a proportional increase in risks.

Let's take an example. Suppose I have a portfolio: 50% in $FF, 30% in more stable tokens, 20% in tokenized real-world assets. The volatility $FF is high — we see this on the chart, where MA(7) is at 0.11347, MA(25) — 0.11437, MA(99) — 0.11413, and they are all located close to each other, indicating a period of consolidation after sharp movements. But the stable part of the portfolio compensates for these fluctuations. As a result, I do not need to hold 200% collateral — 140-150% is sufficient, and I already get much more liquidity for every dollar invested.

Here’s another important point: in traditional protocols, your capital just sits there. You do not earn income from it while it is in collateral. But a properly built infrastructure allows your collateral assets to continue generating income — through staking, farming, or other mechanisms. This is a whole different level of efficiency. You have not only unlocked part of the value of your assets through USDf, but you are also earning income from the collateral. Double benefit.

Look at the current situation with volumes: the hourly trading volume is 4,088,941.6 units, with MA(5) for volume showing 1,235,767.8, and MA(10) — 909,380.7. This indicates that there has been a recent surge in activity — see this huge red column on the volume chart? This is a panic sell-off when the price fell from 0.11797 to 0.11003. In a traditional system with low capital efficiency, such a movement would lead to mass liquidations because people would not have a safety margin.

But if your system is built correctly, if it takes risks into account while maximizing capital utilization, you can survive such drawdowns. I always say: capital efficiency is not about squeezing the maximum from the system at any cost. It is about finding the optimal balance between risk and return. And this is where #FalconFinance offers a solution that was previously unavailable.

Another aspect that is often overlooked is opportunity cost. When you keep 60-70% of your capital in non-working collateral, you lose the ability to use that money elsewhere. Maybe an interesting farming pool with high yields has appeared. Perhaps you saw a profitable investment opportunity. But your hands are tied — capital is frozen. If your efficiency were higher, if you only needed to keep $6,000 in collateral to get the same liquidity instead of $10,000, you would have $4,000 of free funds to maneuver.

I look at the chart and see a classic example of how market cycles work. After a sharp rise to 0.11797, a correction began — this is normal; the market cannot grow forever. But note: after falling to 0.11003, the price has already begun to recover, now at 0.11077. For those who maintain positions with a good safety margin, this is just another fluctuation. For those who operated on the edge with minimal collateral — this could have been liquidation.

And here another advantage of high capital efficiency in a well-structured system manifests: you can afford to maintain a reasonable safety margin without sacrificing a significant part of available liquidity. There’s no need to choose between "safe but inefficient" and "efficient but risky." There’s a third way — smart protocol architecture that takes into account different types of assets, their correlations, liquidity, and risks.

I have come up with a simple rule for myself: if a protocol offers me to use only 30-40% of my collateral's value, it is either too conservative or poorly designed. Modern technologies, smart price oracles, dynamic risk models — all of this allows you to safely raise the bar to 60-70% with reasonable risk management. And this is exactly what @falcon_finance does — provides infrastructure where your capital works with maximum efficiency while the system remains resilient to market shocks.

Do you know what finally convinced me? When I calculated the real yield considering alternative costs. If I keep collateral in a traditional protocol with a 200% ratio, I receive USDf, use them at 5% annual interest, my effective yield on the entire capital is only 2.5% (because only half of the money is working). But if I can get the same USDf at a 140% ratio, my effective yield is already 3.6%. The difference seems small, but over time and with large amounts, it turns into serious money.

Capital efficiency in DeFi is not just a technical term; it is the ability for your money to really work for you, rather than hanging as dead weight waiting for a hypothetical black swan. And the better the protocol addresses this issue, the more attractive it becomes for serious users who count every percentage of yield and every dollar of locked capital.

#FalconFinance @Falcon Finance $FF