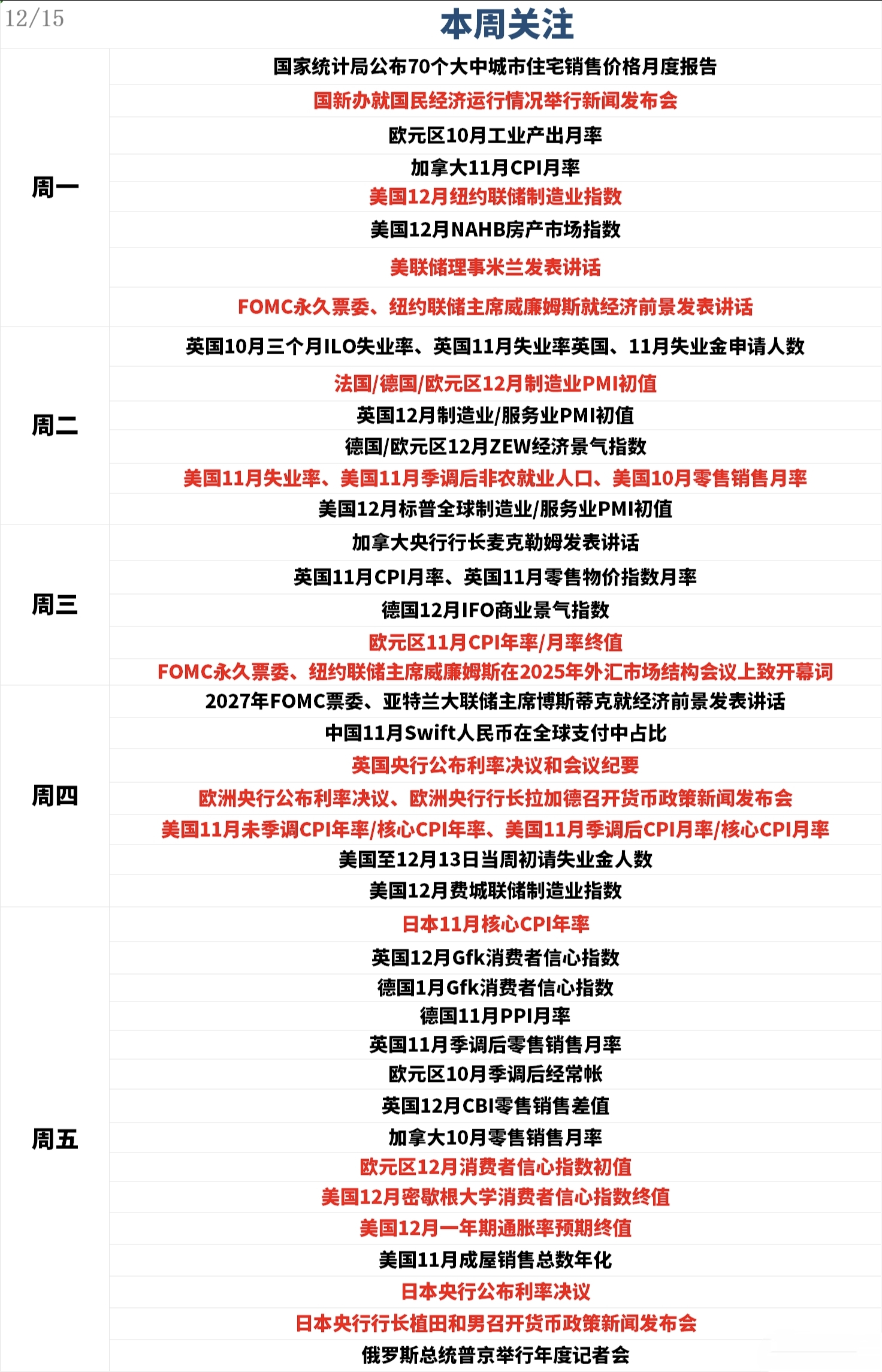

This week, the financial market will welcome a true 'Super Week', where the intensive decisions of global central banks and significant economic data form a 'double kill' combination. The key support level of the US dollar index is precarious, and whether gold and silver can take this opportunity to break through the US dollar's lifeline becomes the market's most core suspense.

Central Bank Nuclear Bomb Group: The Decisions of Three Major Central Banks Stir the Market

This week, four major central banks will successively announce their interest rate decisions, among which the decisions of the European Central Bank, the Bank of England, and the Bank of Japan are considered 'nuclear level', directly influencing the strength and weakness of the US dollar and non-US currencies, thereby affecting gold and silver pricing.

European Central Bank: On Thursday, the interest rate decision will be announced along with a press conference. Currently, inflation in the Eurozone is showing a downward trend, and whether the final value of the November CPI can confirm the trend of cooling inflation will determine whether the ECB releases signals for rate cuts. If the ECB leans dovish, a weaker euro may briefly boost the dollar, suppressing gold and silver; conversely, hawkish statements driving a euro rebound will put pressure on the dollar and open up upward space for gold and silver.

Bank of England: On the same day, the interest rate decision and meeting minutes will be announced, and the performance of the UK November CPI and retail data will become an important reference for the Bank of England's decision-making. UK inflation remains sticky, and if the central bank maintains a hawkish stance, a stronger pound will weaken the dollar's advantage, benefiting gold and silver; if rate cut expectations are released, a pullback in the pound may create short-term pressure on gold and silver.

Bank of Japan: On Friday, the interest rate decision was announced, and Governor Kazuo Ueda's press conference speech is crucial. The market's expectation for the Bank of Japan to exit its negative interest rate policy continues to heat up. If this decision signals a policy shift, the yen's significant appreciation will trigger a decline in the US dollar index, and gold and silver are expected to gain strong upward momentum; if it maintains easing, a weak yen may briefly support the dollar, while gold and silver will need to rely on other favorable factors to break through.

Additionally, the intensive speeches by Federal Reserve officials cannot be ignored. Comments from New York Fed President Williams and other voting members will further reinforce the market's judgment on the pace of Federal Reserve rate cuts, becoming an 'invisible driving force' in the game between the dollar and gold and silver.

Data double whammy: Non-farm payroll + CPI ignite volatility

The US November non-farm payroll and CPI, two core data points, will make their appearances in succession, serving as a 'touchstone' for assessing the fundamentals of the dollar and setting the short-term tone for gold and silver trends.

Non-farm data (Tuesday): As a 'barometer' of the US job market, the combination of unemployment rate, non-farm employment population, and retail sales data will directly reflect the resilience of the US economy. If employment data is weak, coupled with a decline in retail sales, market expectations for the Federal Reserve to cut rates ahead of schedule will heat up, and the dollar index is likely to test key support, providing an opportunity for gold and silver to rise; if the data is unexpectedly strong, hawkish expectations for the Federal Reserve will return, and a stronger dollar will suppress the gains in gold and silver.

CPI data (Thursday): The unadjusted CPI and core CPI data for November are core indicators for judging the inflation trend in the US. If inflation continues to retreat, it will further solidify expectations for rate cuts, putting the dollar's lifeline to a substantive test, and gold and silver are expected to break through key resistance; if inflation rebounds, the dollar index may experience a rebound, while gold and silver may enter a correction.

At the same time, CPI data from the Eurozone, UK, and Japan will be released simultaneously, and changes in the global inflation pattern will constrain the dollar from the peripheral markets, amplifying the volatility of gold and silver.

Gold and silver trends: Can they break through the dollar's lifeline?

Currently, the US dollar index is at a key support range. This week's central bank decision and the combination of heavyweight data will determine whether it can hold its lifeline. For gold and silver, the bulls have two major advantages: first, under the divergence of global central bank policies, the Federal Reserve's expectation of rate cuts is ahead of the European and British central banks, and the logic of a weakening dollar in the medium to long term remains unchanged; second, geopolitical risks and market risk aversion provide underlying support for gold and silver.

If this week's non-farm payroll and CPI data both show weakness, combined with the European and Japanese central banks releasing hawkish/policy shift signals, the US dollar index is likely to break through key support, and gold is expected to challenge the $2100 per ounce mark, with silver also following suit to gain ground. Conversely, if the data is strong and the central bank decision leans hawkish, gold and silver may experience a short-term pullback, but in the medium to long term, the onset of the Federal Reserve's rate cut cycle will still provide upward momentum for gold and silver.

Overall, this week's market volatility is expected to soar significantly. Whether gold and silver can leverage this to break through the dollar's lifeline depends on the 'combined direction' of data and central bank decisions. Investors should be wary of extreme market fluctuations and take appropriate risk hedging measures.