Do you know what has always annoyed me in debates about stablecoins? People are divided into two camps: some fanatically believe in centralized USDT and USDC, while others shout that only decentralized DAI has the right to exist. And I sit and think: why do we even have to choose? Why can't we look at each option soberly, understand the pros and cons, and use what fits your situation? When I started to understand USDf from @falcon_finance, I realized that this is not just another stablecoin in a long list — this is a different approach to how synthetic dollars should work. Let's analyze all three options honestly, without fanaticism.

Let's start with USDT because it's the oldest and largest player. Tether has been around since 2014 and has gone through many scandals, accusations, and investigations during this time. I've personally used USDT for years, and I have mixed feelings about it. On one hand, it's the most liquid stablecoin in the world—you can exchange it on any exchange, anywhere on the planet, often with the least slippage. If I need to quickly exit a position or move funds between exchanges, USDT is the obvious choice simply because of pure liquidity.

But there’s a huge 'but'. Tether is a centralized company that claims every USDT is backed by dollars and equivalents in their reserves. But how much can we trust them? The history of concealing losses, opaque audits, constant changes in reserve structure (sometimes cash, sometimes commercial papers, sometimes something else)—all of this raises concerns. If Tether were found partially unbacked tomorrow and a depeg happened, millions of people would lose money instantly. This is a systemic risk that always exists as long as you hold USDT.

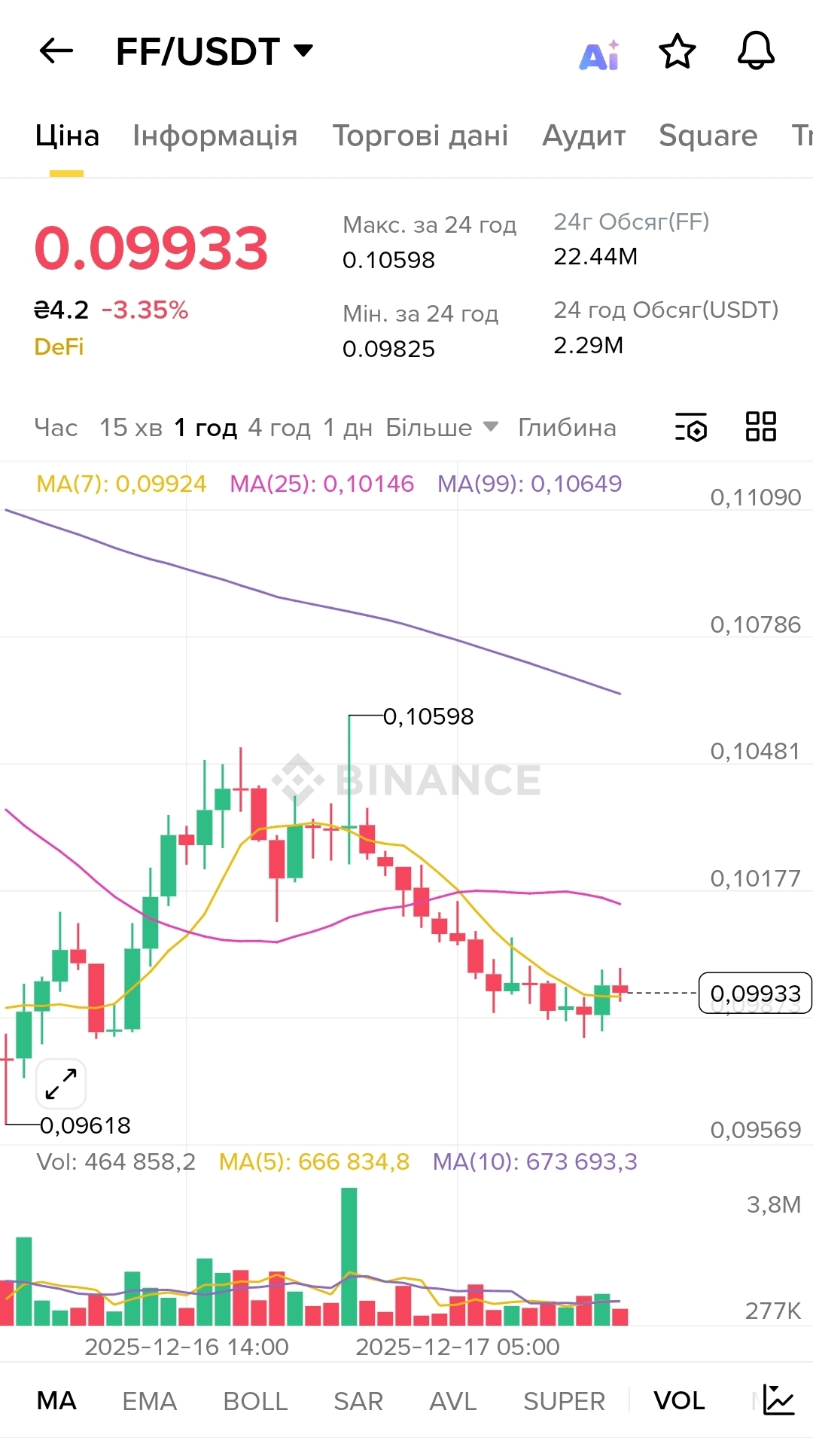

Look at the current chart $FF —price 0.09933 USDT, down 3.35% in a day. Over the last 24 hours, the maximum was 0.10598, the minimum 0.09825—a fluctuation of 7.9%. It’s precisely because of such volatility that people seek refuge in stablecoins. But if your 'safe' stablecoin itself has a risk of implosion due to centralization, that's not a very good refuge, is it?

Now about USDC from Circle. It's a more 'respectable' option—a company registered in the USA, regular audits from major firms, a transparent reserve structure (mostly cash and short-term US treasury bonds). I trust USDC more than USDT when it comes to collateral. They really hold dollars one-to-one, and that's confirmed by independent auditors. Plus, if you're working with American platforms and services, USDC is often better integrated than others.

But again—this is a centralized company. And here's what matters: Circle has already shown that it can freeze tokens at the direction of regulators. This happened with addresses associated with Tornado Cash. Regardless of whether you agree with such actions from an ethical standpoint, the fact remains: your USDC can be frozen without your consent if some institution decides you violated something. For some, this is an acceptable compromise for safety and regulation. For me, who values financial freedom and independence, it's a red flag.

Look at the moving averages: MA(7) at 0.09924, MA(25) at 0.10146, MA(99) at 0.10649. All three lines are below the current price... wait, mistake—the current price of 0.09933 is actually below all the averages. This confirms that we are still in a downtrend. And this is where the value of a truly decentralized stablecoin manifests: when the crypto market is falling and everyone is panicking, you want to be sure that your stablecoin won't disappear along with everything else due to someone's mistake or abuse in a centralized company.

And now let's talk about USDf from #FalconFinance. It's a synthetic stablecoin with over-collateralization, philosophically similar to DAI from MakerDAO, but with several key differences. First, USDf is issued against not only cryptocurrencies but also tokenized assets from the real world. This means greater stability of collateral—not all of it correlates with the volatile crypto market. If Bitcoin drops by 20%, but your tokenized real estate remains stable, the overall risk profile is much better.

Secondly, over-collateralization. To issue USDf at $1000, you need to collateralize assets worth $1500-2000 depending on their type. This means that even if the price of collateral drops by 30-40%, the system remains solvent. Compare this with USDT or USDC, where theoretically every dollar is backed by one dollar, but in practice, you just take the company's word for it. With USDf, collateral is verified on the blockchain in real-time, it's transparent, and can be seen by everyone.

I'm looking at trading volumes—22.44 million per day for the token and 2.29 million USDT—and I understand the difference in scales. USDT trades in billions daily. This is a huge advantage in terms of liquidity, but it also represents a massive concentration of risk. If USDT drops, the entire market shakes. USDf is still smaller, which means lower liquidity, but it also means greater flexibility, more decentralization, and less systemic risk for the entire ecosystem.

The third advantage of USDf is universal collateral infrastructure. You can use a wide range of assets as collateral, not limited to a few approved tokens like in MakerDAO. Want to collateralize $FF? No problem. Want to add tokenized gold? Great. Have tokenized real estate? Also accepted. This flexibility makes USDf more adaptable to various user needs.

The current hourly trading volume is 464,858.2 units, with MA(5) showing 666,834.8, and MA(10) at 673,693.3. Do you see that big green bar in the past on the volume chart? That was the moment when someone big decided to enter a position. For a small token, such moves can create volatility. But for a stablecoin that is over-collateralized, it's less of an issue—the price of USDf remains stable regardless of what happens with the underlying token $FF.

What about DAI? That's a fair question because DAI from MakerDAO is classic decentralized stablecoin. I respect what they've built; it's truly a revolutionary product. But DAI has its issues. Over time, MakerDAO has added more centralized assets (USDC) to its reserves to maintain stability. Now a significant portion of DAI's collateral is actually USDC. This means that 'decentralized' DAI actually relies on centralized USDC. Irony, right?

USDf from @falcon_finance tries to avoid this trap by focusing on truly decentralized and diverse collateral assets. Of course, the protocol is younger, less time-tested, and has less liquidity. But the philosophy is right: true decentralization, transparency, over-collateralization, universality.

Look at the current price of 0.09933 and compare it with the maximum of 0.10598 for the day—a drop of 6.3%. If all my capital were in $FF, it would be painful. But if I use $FF as collateral to obtain USDf, and keep USDf as a stable asset or use it for earning, my exposure to this volatility is significantly lower. This is the beauty of over-collateralized synthetic stablecoins—they provide stability when everything around is fluctuating.

Now let's be honest about the downsides. USDT and USDC have enormous liquidity, wide acceptance, integration literally everywhere. USDf is still significantly smaller; it's accepted by fewer platforms, liquidity pools are thinner. If you need to move quickly between different ecosystems or exchange large amounts, USDT/USDC are currently better options simply due to scale.

USDT and USDC also have a simpler mental model: 1 token = 1 dollar in the company's bank (theoretically). USDf requires understanding the mechanics of over-collateralization, liquidation risks, and collateral dynamics. It's not complicated, but it poses an additional cognitive barrier that deters newcomers.

But here's what I've learned over the years in crypto: convenience and liquidity are great, but they shouldn't be the only criteria for selection. Systemic risk, centralization, and the potential for censorship all matter. And if we're building a truly decentralized financial system, we need tools that embody these principles, even if they're currently smaller and less convenient.

Look at MA(99) at 0.10649—this is a long-term benchmark for $FF. The current price of 0.09933 is 6.7% lower. For a protocol building long-term infrastructure, what's more important is not the immediate token price but the fundamental value of what it offers. And if USDf really becomes a bridge between traditional assets and DeFi, between centralization and decentralization, between volatility and stability—its place in the market is guaranteed.

My personal choice in 2025? I use all three. USDT for quick moves between exchanges when maximum liquidity is needed. USDC for interacting with regulated platforms and American services where it is best integrated. And USDf for long-term storage and as a basis for passive income strategies, because here I control my assets, see the collateral, and no one can freeze my funds at a regulator's call. Diversification—not only among different tokens but also among different types of stablecoins—is a wise approach in a world where no option is perfect. And when someone asks me, 'Which stablecoin to choose?', I reply, 'Why choose one? Use the one that fits the specific task and understand the risks of each.'

#FalconFinance @Falcon Finance $FF