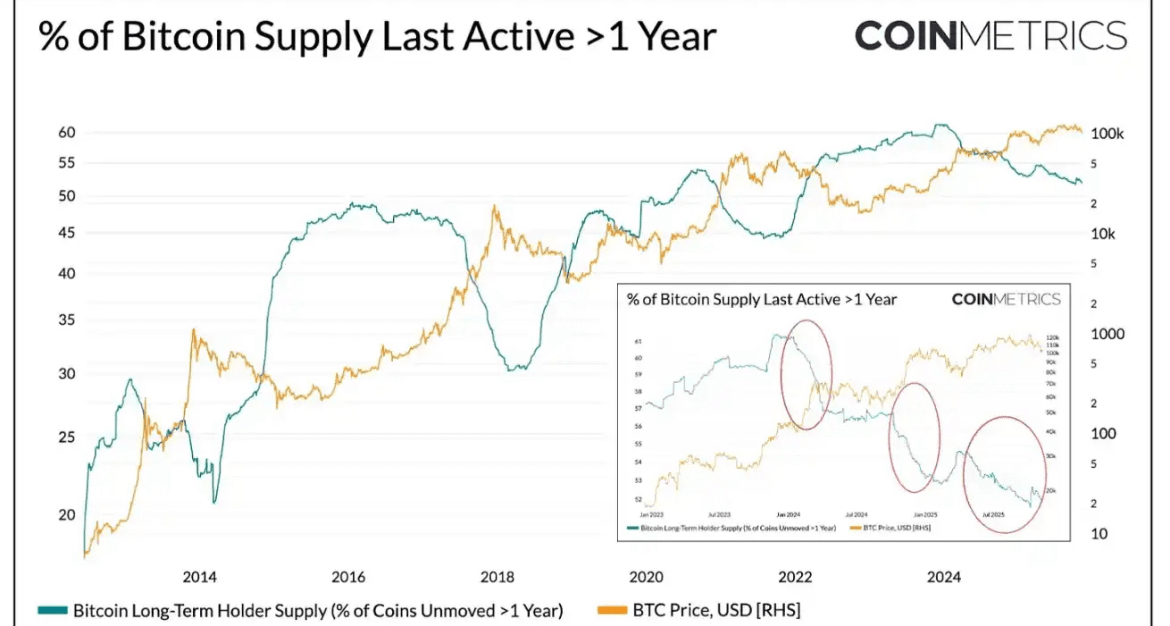

As of now, out of 19.94 million Bitcoin in circulation, nearly 52% of the tokens have not moved for over a year, which is down from the figure of 61% at the beginning of 2024. Whether it is the growth rate during the bear market or the decline rate during the bull market, both have stabilized significantly. Transaction pushes were observed in the first quarter of 2024, the third quarter of 2024, and recently in 2025. This indicates that long-term holders are selling their tokens in a more sustainable manner, reflecting an extension of the ownership transfer cycle.

ETF and DAT: The fundamental drivers of demand

In contrast, since 2024, the supply from short-term holders (tokens active last year) has steadily increased, as previously dormant tokens return to trading. Meanwhile, with the launch of spot Bitcoin ETFs and the accelerated accumulation pace of the digital asset treasury (DAT), new and sustainable demand has emerged, absorbing the supply distributed by long-term asset holders.

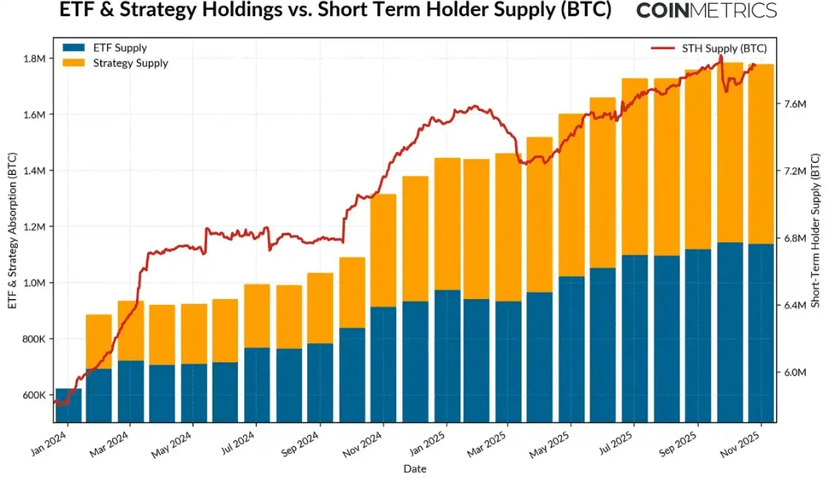

As of November 2025, the number of active Bitcoins last year is 7.83 million, an increase of 34% from 5.86 million in early 2024 (the re-trading of dormant tokens). During the same period, the holdings of Bitcoin ETFs and spot strategies grew from approximately 6,000,000 Bitcoins to 1.9 million Bitcoins, representing nearly 57% of the net increase in supply from short-term holders. Currently, these two channels together account for about 23% of short-term holder supply.

Despite the recent slowdown in inflows over the past few weeks, the overall trend indicates that supply is gradually shifting towards more stable and longer-term holding channels, a unique characteristic of the market structure in this cycle.

Short-term and long-term holder behavior

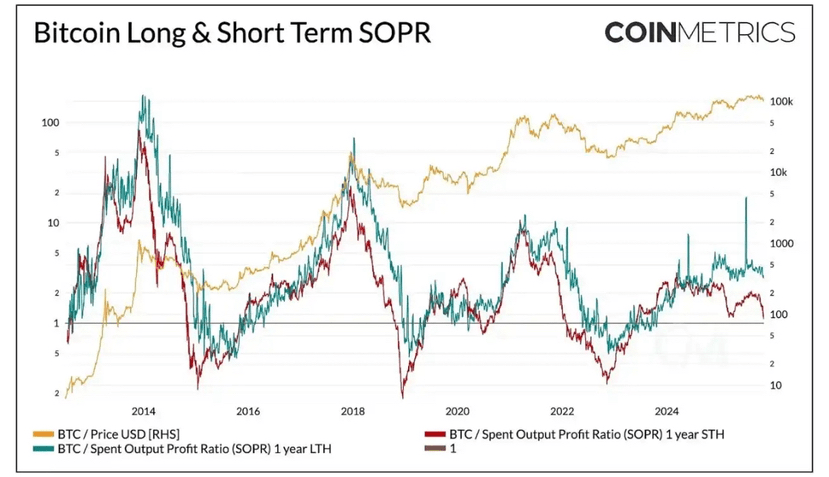

The actual profit trend also confirms the gradual nature of Bitcoin's supply dynamics. The Spending Profit Ratio (SOPR) is used to measure whether holders are selling their tokens at a profit or a loss, providing a clear reflection of the behavioral patterns of different holder groups throughout the market cycle.

In previous cycles, profit-taking behaviors of long-term and short-term holders often displayed severe and simultaneous volatility. However, recently, this relationship has diverged: the SOPR for long-term holders remains slightly above 1, indicating steady profit realization and moderate selling at its peak.

The SOPR for short-term holders hovers around the breakeven line, explaining the recent cautious market sentiment as many short-term holder positions are close to their cost basis. The difference in behavior between these two types of holders reflects the current state of greater stability in the market: institutional demand has absorbed the supply distributed by long-term holders, moving away from extreme volatility in the past. If the SPR for short-term holders continues to exceed 1, it may indicate strengthening market momentum.

While the significant pullback will continue to pressure the ability to generate profits for all holding groups, the overall pattern indicates a more balanced market structure: supply turnover and profit-taking are gradually advancing, expanding the rhythm of the Bitcoin cycle.

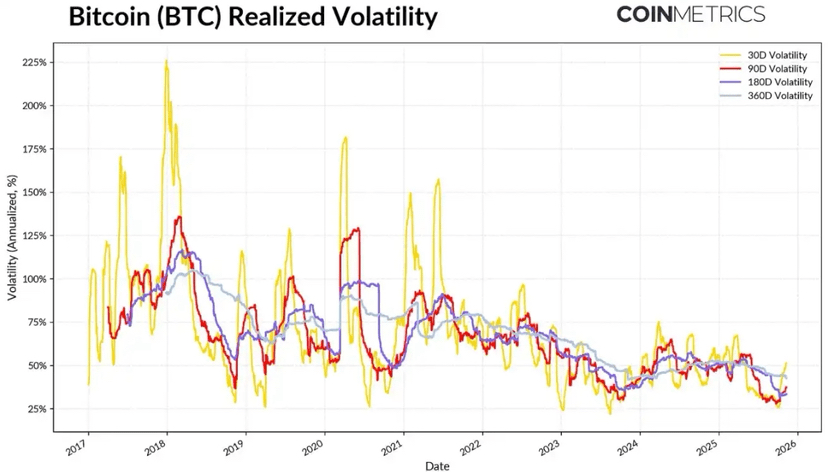

Declining Bitcoin volatility

This structural stability is also reflected in the volatility of Bitcoin, which has been on a downward trend. Currently, the actual volatility of Bitcoin over 30 days, 60 days, 180 days, and 360 days remains stable around 45%-50%, while its volatility in the past was often explosive, leading to significant market fluctuations. Now, the characteristics of Bitcoin's volatility increasingly resemble those of large tech stocks, indicating its maturation as an asset. This not only reflects improved liquidity but also confirms that institutional investors have become a significant force in the market.

For asset allocators, declining volatility may enhance Bitcoin's appeal in portfolios, especially as its correlation with macro assets such as stocks and gold continues to evolve.

Conclusion

Bitcoin's on-chain trends suggest that this current cycle is progressing into a smoother and longer phase, without the frenzied price movements seen in previous bull markets. Long-term holders are gradually offloading their holdings, with much of it being absorbed through more sustainable demand channels such as ETFs, DCA, and broader institutional holdings. This shift indicates a mature market structure: reduced volatility and trading speed, alongside extended cycles.

However, market momentum still relies on the sustainability of demand. ETF flows are plateauing, some DCAs are facing pressure, and recent market-wide liquidation events, alongside the short-term SOPR hovering around breakeven levels, highlight the market in a phase of re-adjustment. An uptick in supply held by long-term holders (tokens not moved for over a year), a break of SOPR above 1, and inflows into spot Bitcoin and stablecoin ETFs could be key signals for the return of market momentum.

Looking ahead, reducing overall uncertainty, improving liquidity conditions, and regulatory progress related to market structure could reignite capital flows and extend the bull market cycle. Despite the cooling market sentiment, following a recent debt adjustment, supported by institutional expansion and advancements in on-chain infrastructure, market fundamentals are stronger.