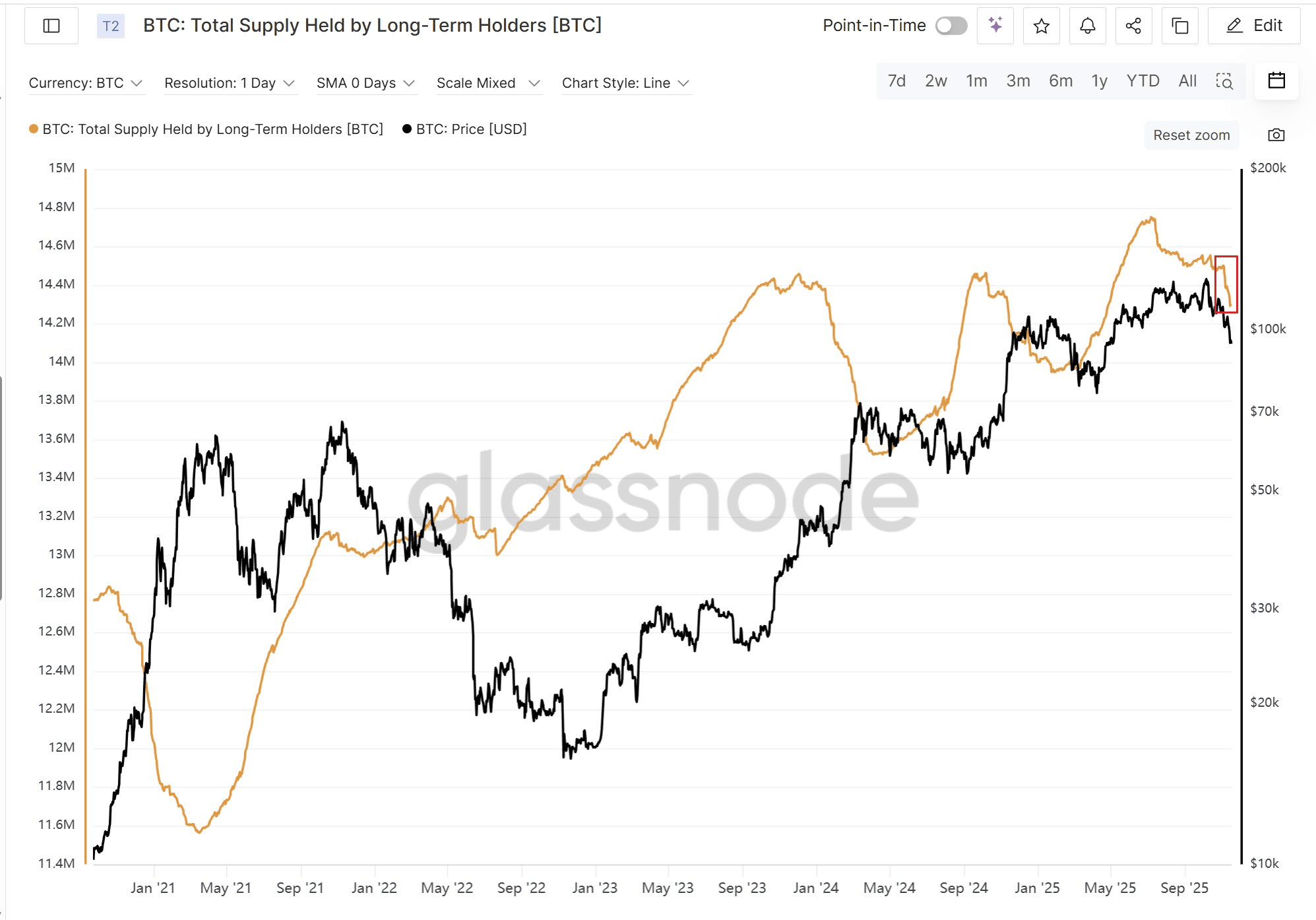

Recently, the number of chips held by long-term holders (holding coins for approximately more than six months) has declined synchronously with the #BTC price, which is an atypical situation 👇

Generally speaking, long-term holders often sell off profits during the price increase due to substantial floating profits and choose to remain dormant during the price decline.

Let's analyze which long-term holders are still selling during the decline in cryptocurrency prices.

Investors holding coins on-chain for 3-5 years recently experienced a single-day sell-off of $4.37 billion, but this is likely the action of a single entity and not representative of the broader trend (this image is omitted due to the limit on the number of inserted images).

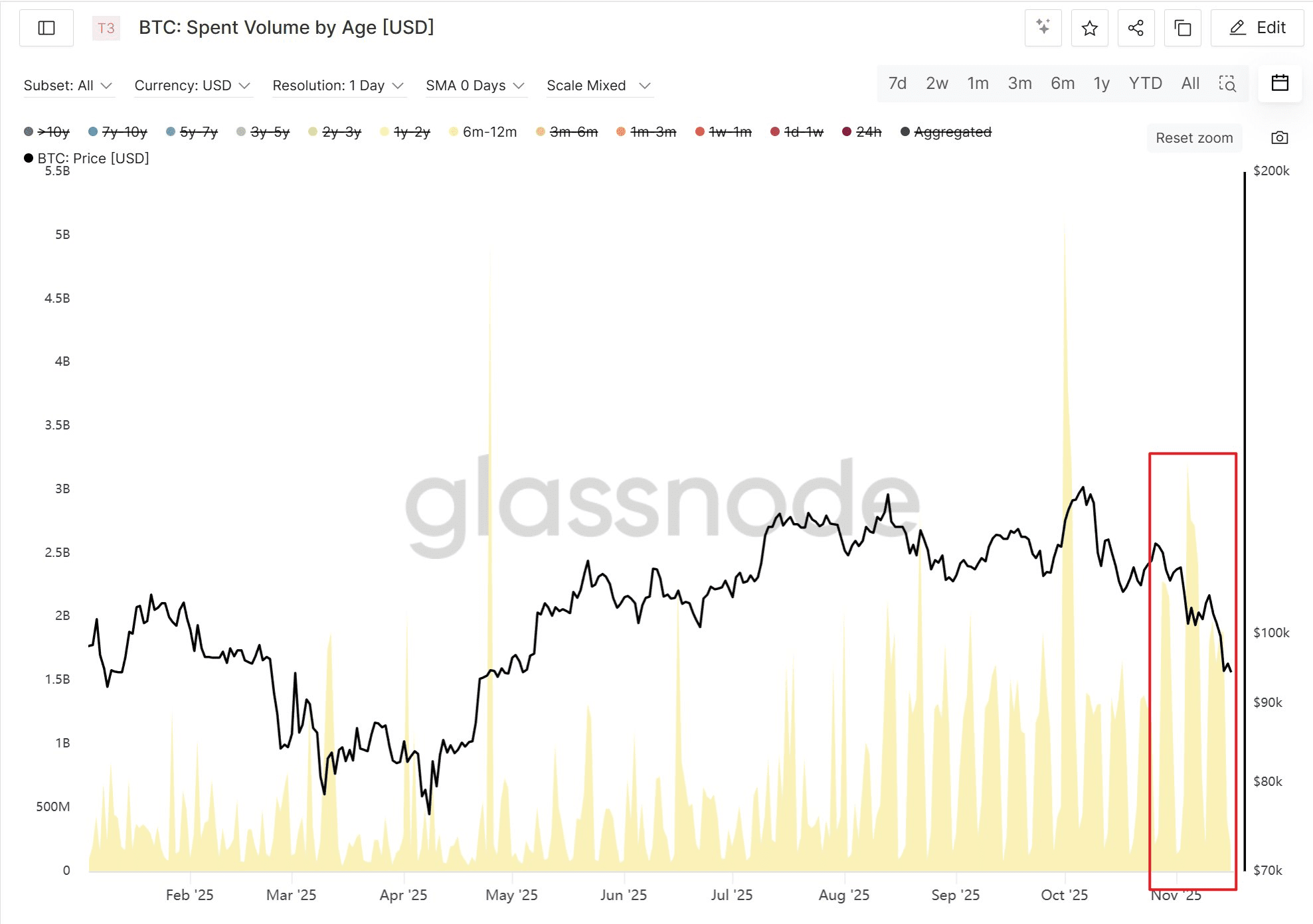

In addition, investors holding coins on-chain for 6-12 months have recently sold a large number of chips. They are the main force behind the continuous selling of chips despite the recent decline in cryptocurrency prices 👇

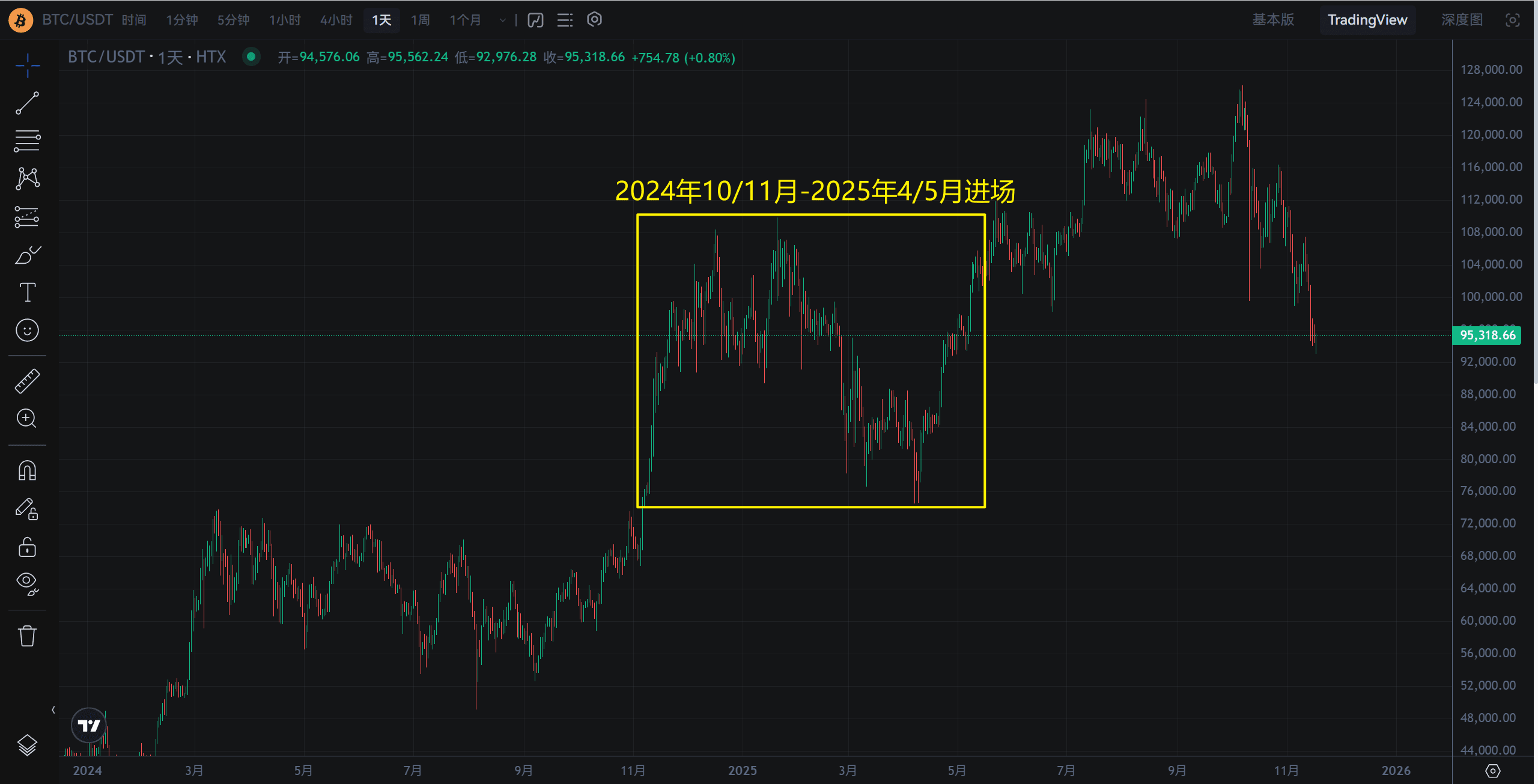

Estimating, this group of investors who have held coins for 6-12 months entered the market around October/November 2024 to April/May 2025 👇

It can be seen that the main body of this group of investors is those who were trapped at prices above $90,000/$100,000 at the end of 2024 and early 2025. The recent decline in cryptocurrency prices has repeatedly reached or even fallen below the entry cost of these investors. Due to unwillingness to bear greater losses, they choose to sell their chips to exit with minimal or no loss. This is the main reason for the recent synchronous decline in the number of chips held by long-term holders and the cryptocurrency price.

Coincidentally, historically, after the $69,000 peak in 2021, the number of chips held by long-term holders also declined synchronously with the cryptocurrency price 👇

The logic behind this is similar to the current situation, where a significant amount of chips were trapped at the first peak of the double top (the first half of 2021 when the cryptocurrency price was $60,000+), and then during the subsequent decline after the second peak of the double top, the trapped chips at the first peak could no longer endure the losses and sold their chips.

Conclusion:

The underlying logic of the atypical chip selling behavior of long-term holders recently is similar to that after the $69,000 peak in 2021, but this does not mean that the future will certainly enter a major bear market like it did after the $69,000 peak in 2021.

First of all, the active selling of trapped chips at the end of 2024 and early 2025 will not continue indefinitely. If the continuous decline in cryptocurrency prices leads to the bubble being squeezed out, the atypical selling behavior of this group of investors will gradually return to normal.

Secondly, the major bear market after the $69,000 peak in 2021 was strongly correlated with the decline of the U.S. stock market and the global financial market at that time, and the situation then cannot be mechanically applied to the current context.

The focus in the next 2-3 months should be on when the active selling of profit chips will slow down, and when the market bubble will be completely squeezed out as the price may continue to decline. Continuing to patiently wait for a better entry opportunity is a suitable choice for the near future.