Key takeaways

Twenty One Capital’s NYSE debut saw a nearly 20% drop, signaling cautious investor sentiment toward Bitcoin-heavy public listings.

XXI traded close to its net asset value, suggesting the market did not assign a meaningful premium beyond the value of the firm’s Bitcoin holdings.

The decline reflected broader market pressures, including Bitcoin volatility, fading enthusiasm for SPAC-backed listings and weakening mNAV premiums.

The muted reaction suggests investors may now expect Bitcoin-focused firms to show clear, durable revenue models rather than relying primarily on large BTC holdings.

The public debut of Twenty One Capital, a closely watched Bitcoin-focused company, on the New York Stock Exchange (NYSE) was met with cautious investor sentiment. Trading under the ticker XXI, the firm’s shares fell by nearly 20% on its first day.

This article explores what the market reaction may signal about shifting investor demand, the erosion of the mNAV premium and the broader scrutiny facing Bitcoin-backed equity listings.

What Twenty One Capital actually is

Twenty One Capital is an institutionally backed, Bitcoin-native public company with the stated ambition of becoming the largest publicly traded holder of Bitcoin (BTC). The firm went public via a special-purpose acquisition company (SPAC) transaction with Cantor Equity Partners and began trading under the ticker XXI.

At launch, the company reported a treasury of over 43,500 BTC, valued at roughly $3.9 billion-$4.0 billion, placing it among the largest corporate Bitcoin holders.

The firm was built with a clear focus: a corporate structure that places Bitcoin at the center of its strategy. Its founders and backers position it as more than a treasury vehicle. Jack Mallers, who also founded Strike, has said that Twenty One aims to build corporate infrastructure for Bitcoin-aligned financial products.

This model places Twenty One alongside other digital asset treasury (DATs) companies, but with key differences. Its backers include Cantor Fitzgerald, a Federal Reserve primary dealer; Tether, the issuer of USDt (USDT) and a major holder of US Treasurys; Bitfinex and SoftBank. These institutional relationships position Twenty One as one of the most heavily backed Bitcoin-native companies to list publicly.

The company arrived amid a broader wave of publicly traded firms pursuing Bitcoin-centric strategies, inspired in part by the expansion model used by Strategy (formerly MicroStrategy). Still, Twenty One’s stated intention is not simply to replicate that approach but to pursue revenue-driven growth while maintaining a large Bitcoin reserve.

The debut and the sharp price drop

Given the scale of its treasury and the profile of its backers, many market participants expected strong attention around Twenty One’s launch. Yet its first day of trading on Dec. 9, 2025, delivered a different outcome. The stock fell sharply despite the company’s large Bitcoin holdings and high-profile institutional support.

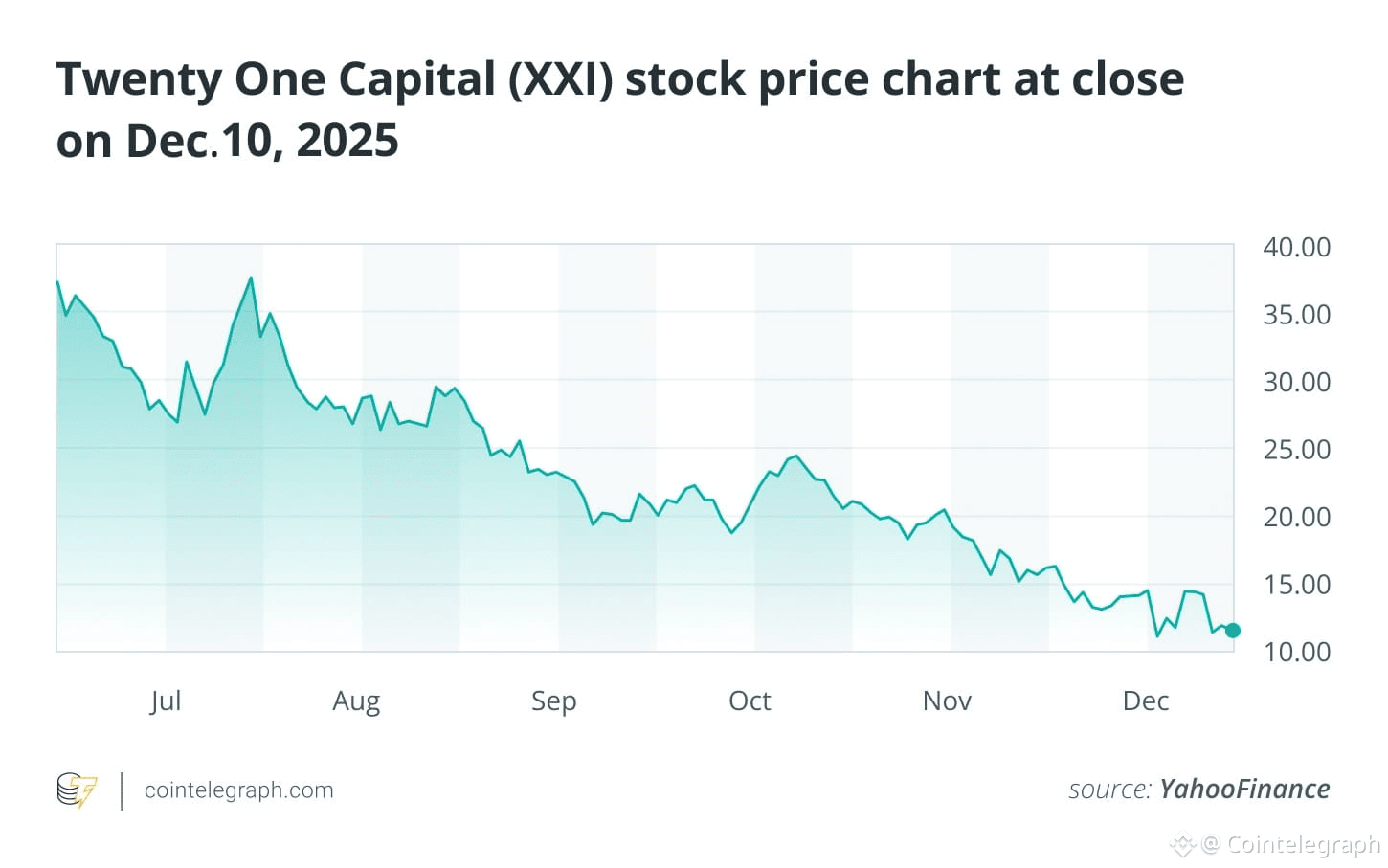

When Cantor Equity Partners’ SPAC shares converted into XXI, the new stock opened at $10.74, below the SPAC’s prior close of $14.27. After-hours trading showed only a modest rebound. By the close of its first day of trading, the shares were down approximately 19.97%, settling at $11.96.

This performance underscored a broader trend in which newly listed crypto-related firms often trade below their pre-merger benchmarks. The move also left the newly public equity trading at a discount relative to its underlying cryptocurrency holdings, indicating that valuation dynamics for this type of stock may be shifting.

Investor caution and Twenty One’s NYSE slide

The sharp decline in Twenty One Capital’s stock price was not unique to the company. It reflected a convergence of three market factors in late 2025:

Erosion of the multiple-to-net-asset-value (mNAV) premium

Continued volatility in crypto markets

Weaker sentiment toward SPAC-driven public debuts.

Understanding the muted mNAV valuation

The clearest sign of market caution was that the stock did not trade at a meaningful premium to the value of its underlying Bitcoin holdings. This is typically assessed using the mNAV ratio.

Historically, Bitcoin treasury firms have commanded a high mNAV premium at points in past market cycles. That premium has often been interpreted as a sign of investor confidence in management’s ability to create value beyond the underlying assets.

Twenty One Capital, however, traded at or near its asset value, effectively assigning little to no premium to its business plans or management. This suggested the market was valuing the stock largely as a direct and potentially volatile proxy for Bitcoin rather than pricing in a distinct operating-business premium.

Market volatility and SPAC sentiment

Twenty One Capital debuted during a challenging period for both the crypto market and SPAC-driven listings. In the run-up to the debut, cryptocurrencies faced selling pressure. Bitcoin had fallen more than 28% from its October peak, creating a risk-off climate in which investors were less willing to assign generous valuations to crypto-linked equities.

The merger with Cantor Equity Partners was a SPAC-driven route to going public. While the prospect of the deal previously sent the SPAC’s shares sharply higher, by late 2025, enthusiasm for high-profile crypto SPACs had cooled. A long track record of post-merger underperformance has contributed to investor fatigue and skepticism, which can lead newly listed companies to trade below their pre-merger benchmarks.

Did you know? The equity trading below the value of its Bitcoin treasury is an example of a valuation paradox, where a newly public stock trades at a discount to the market value of the primary liquid assets it holds.

Market shift: Demand for proven business models

Another reason for investor caution may be the lack of a clear, proven, revenue-generating operating model at the time of the debut. This suggests some investors may be moving away from pure “Bitcoin treasury” narratives and placing greater emphasis on differentiation and predictable cash flows.

Twenty One Capital went public with large Bitcoin holdings, but without a detailed, publicly available business plan or a confirmed timeline. The debut also came during a period of heightened scrutiny of the digital asset treasury company sector.

According to Reuters, analysts suggest it is becoming “harder for DATs to raise capital” and that companies “need to show material differentiation” to justify their trading multiples.

The sharp drop in XXI’s share price may indicate that the market’s perspective is evolving. Some investors may be shifting their focus toward a company’s ability to execute a sustainable business model alongside its assets. Public markets may increasingly prioritize firms that can generate predictable cash flows rather than those that primarily hold Bitcoin.