The current market phase can be defined as a post–all-time-high adjustment. Directionally, bearish pressure remains conditionally dominant, reflecting demand fatigue rather than panic-driven selling.

In 2025, the U.S. ETF market recorded roughly $1.4 trillion in year-to-date net inflows, with equities and fixed income leading capital allocation.

Crypto-related ETFs played a secondary but notable role. Spot Bitcoin ETFs continued to attract inflows despite Bitcoin posting negative year-to-date performance, suggesting that some investors prioritized long-term exposure over short-term price action. However, traditional equity ETFs remained the primary drivers of overall ETF flows, leaving crypto ETFs structurally peripheral.

Bitcoin’s weaker performance is best explained by structural factors. The ETF adoption narrative was largely priced in by mid-year, limiting incremental demand. Persistently high interest rates constrained risk appetite, while positions accumulated at elevated price levels continued to unwind as the market shifted from expansion to adjustment.

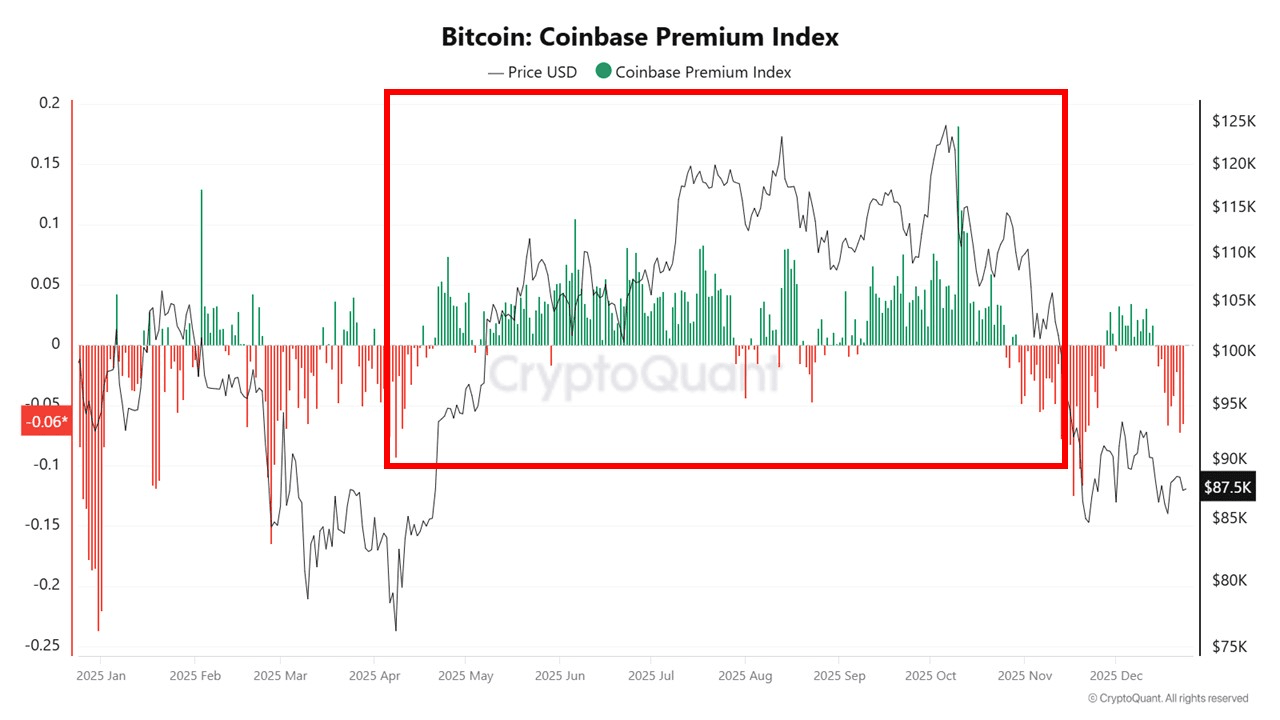

On-chain data supports this view through the Coinbase Premium Index. During the mid-year rally, the premium remained mostly positive, indicating steady U.S.-based demand. More recently, it has turned persistently negative, signaling a weakening of U.S. spot demand rather than aggressive distribution.

This shift does not imply capitulation. Instead, incremental spot demand has been insufficient to absorb existing supply. As the premium deteriorated, price followed lower, suggesting demand exhaustion—not forced liquidation—as the dominant force.

An alternative scenario would require a sustained recovery in the Coinbase Premium Index, signaling renewed U.S. demand and a transition toward re-accumulation.

At present, demand normalization remains the base case, though consistent premium recovery would warrant a reassessment.

(Analysis Report No.156)

The XWIN Group operates the DeFi platform “xwin.finance”.

Written by XWIN Research Japan