Sober Options Studio × Derive.XYZ Joint Production

1. Macroeconomic Noise and the Option Pricing Impact of the TACO Script

Last week, the global financial markets experienced another round of intense volatility driven by macro geopolitical news. This frequently occurring pattern has been humorously dubbed by seasoned traders as 'TACO trading' (Trump Always Chickens Out) — a high-risk, high-reward gambling behavior that is profoundly reshaping the ecological logic of the crypto options market. The so-called 'TACO strategy' is essentially a summary of the U.S. government's erratic behavior in major decision-making: when policies trigger severe market fluctuations or economic pressure, the relevant decision-makers (typical behavior during the Trump era) often tend to quickly release soothing signals or actively retreat. This pattern has formed a clear script loop:

A typical case occurred in April 2025: after the U.S. announced a threat to impose 'reciprocal tariffs' on major trading partners, Bitcoin's maximum drop within 24 hours exceeded 3%, and market panic quickly spread; however, during the subsequent negotiation period, Trump's attitude gradually softened, market sentiment improved, and Bitcoin and other risk assets saw a significant rebound.

Such cycles of 'panic sell-off - policy easing - violent rebound' have been viewed by savvy investors as a golden window to capture 'V-shaped reversals' using options tools. As the script is repeatedly played out, the market has shifted from 'passive response' to 'active prediction', even showing obvious 'running ahead' phenomena—investors betting on reversals in advance, pushing the logic of option pricing to change: tail risk premiums have become dominant factors, and demand for hedging extreme risks has significantly increased, with the options market accelerating its evolution toward a macro high-frequency game model.

II. BTC and ETH Volatility Structure Analysis: A multidimensional mapping of uncertainty

The current pricing structure of the options market clearly reflects the uncertainty brought by macro gaming. We analyze from three key dimensions:

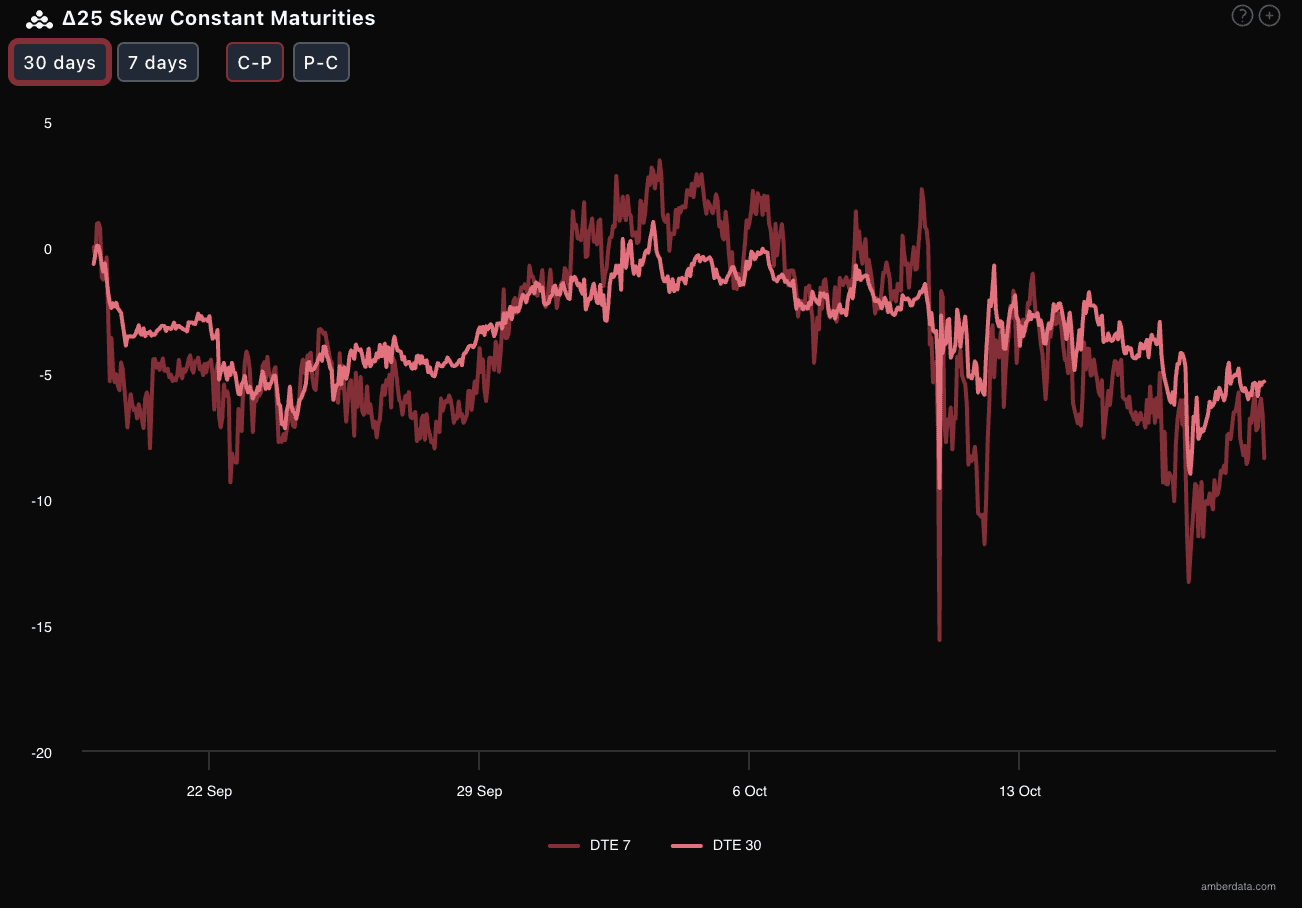

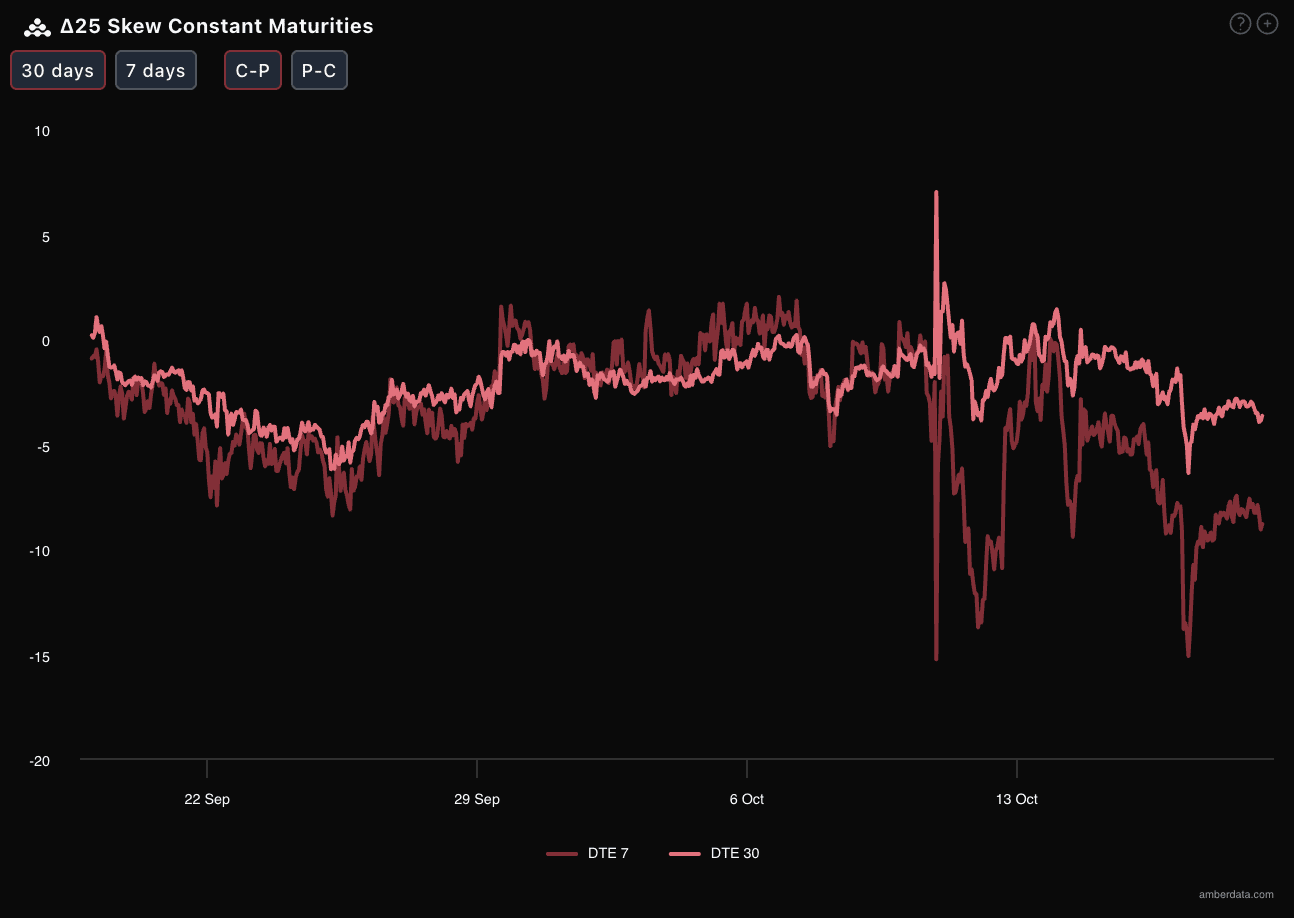

Skew: Short-term panic sentiment outweighs long-term

Observing through Delta 25 Skew (Call Option Implied Volatility IV - Put Option IV): Recently, this indicator for BTC and ETH has generally been in a significantly negative range, indicating that the market assigns higher pricing to downside (bearish) tail risks, and bearish sentiment or demand for downside hedging is extremely strong. More importantly: the negative Skew value for DTE 7 days (contracts expiring in 7 days) is more severe than for DTE 30 days, and ETH's DTE 7 days negative Skew value is far lower than BTC's—this directly points to two conclusions:

In the short term (especially within a week), the market's concerns about sudden macroeconomic news or market 'cleansing behaviors' (such as a sharp drop caused by a liquidity crash) are significantly stronger than in the medium to long term;

The market confidence in ETH is weaker than in BTC, and investors are more vigilant against its extreme short-term declines.

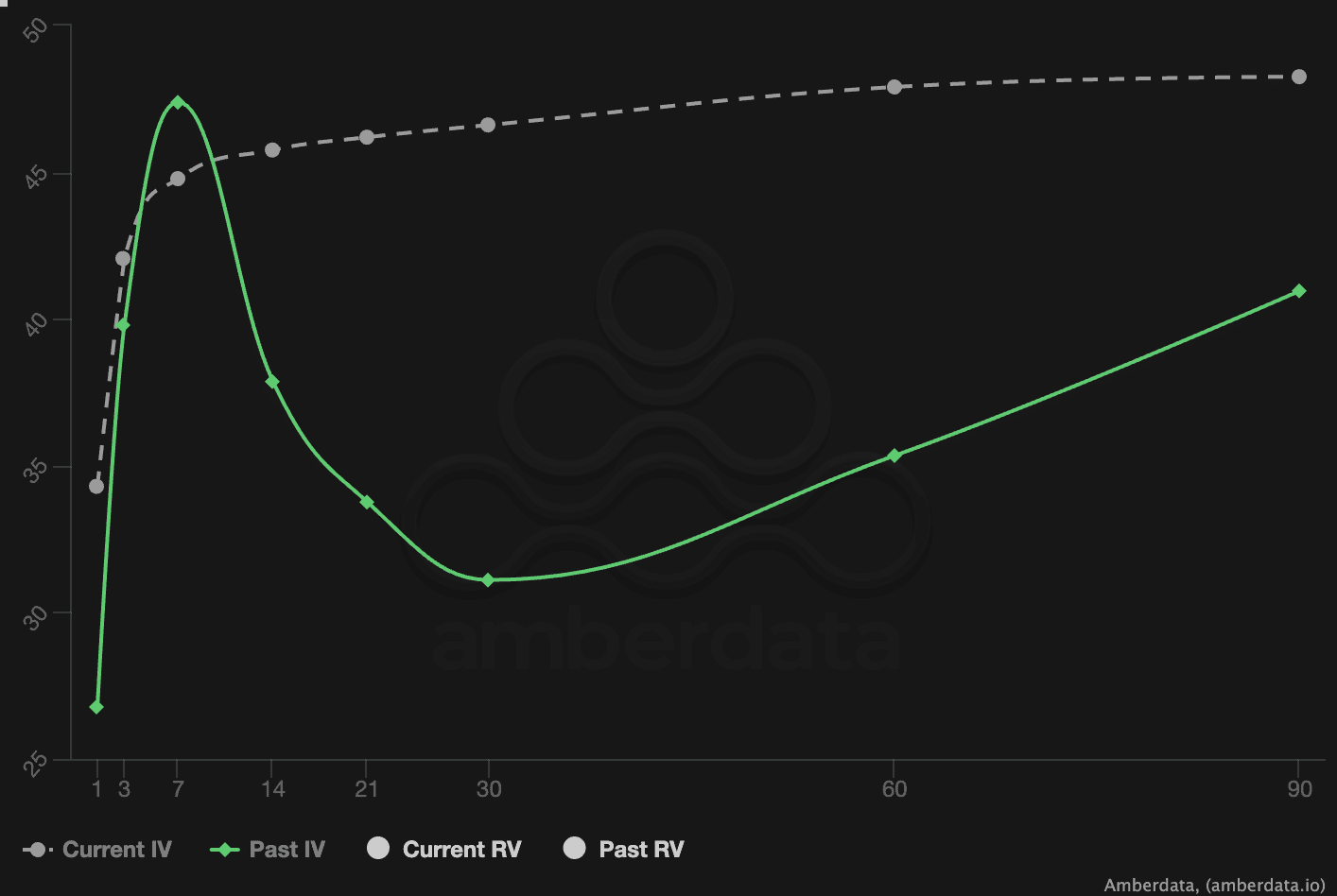

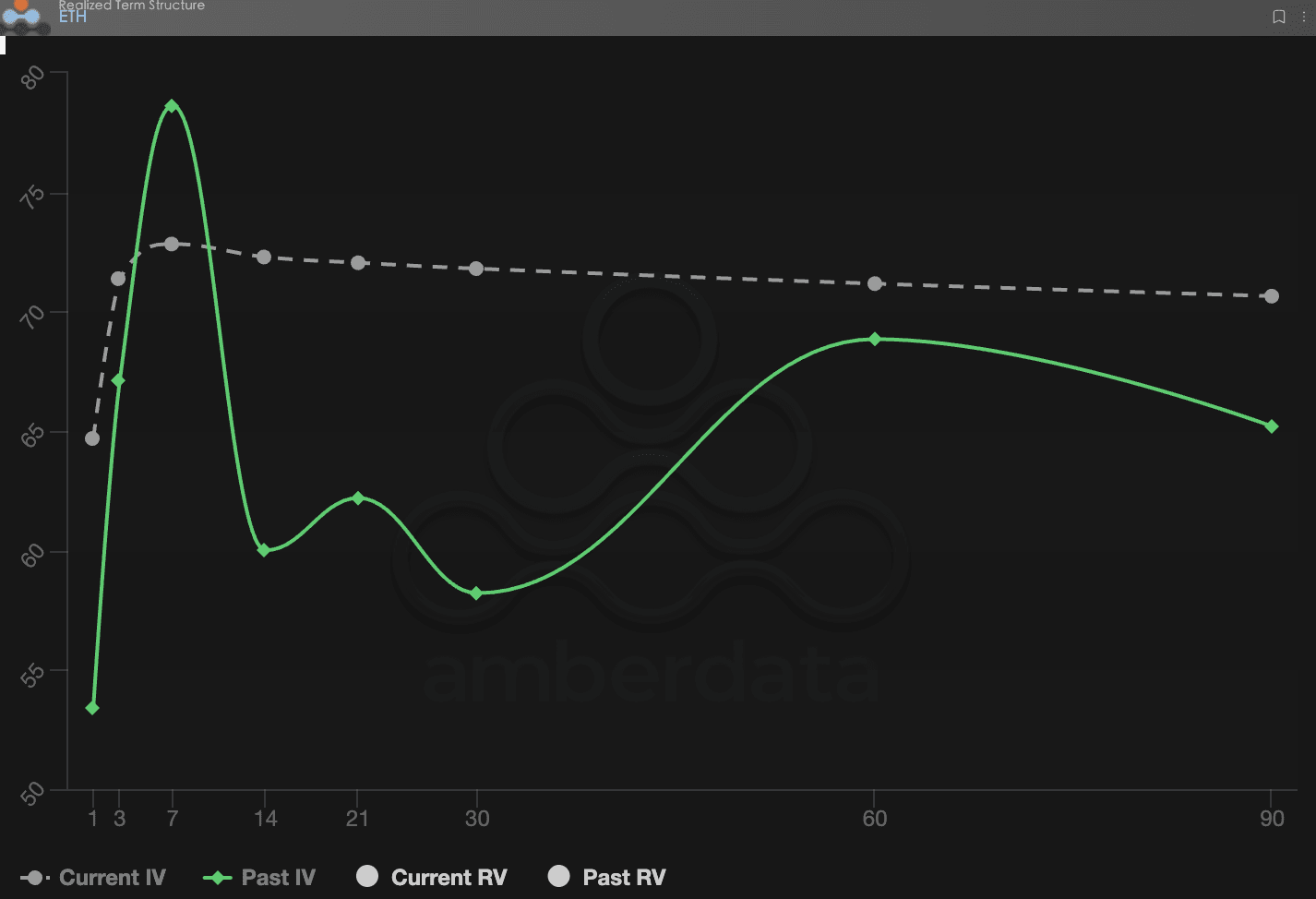

Term Structure: Near-term high pressure and far-term central elevation

The current IV (implied volatility) term structure presents characteristics of 'high near-term and gradual rise in the far term': there is a local peak near DTE 7 days, followed by a slow rise of the curve to higher levels at DTE 90 days. Looking back at Past IV (historical same-period term structure), there has been a clear 'hump' shape—indicating that the market experienced brief but severe short-term volatility at a certain time, leading to abnormally high short-term IV. More critically: the current Current IV at the far end (DTE 60/90) is significantly higher than Past IV, indicating that the market's expectations for the volatility center in the next 3-6 months are systematically rising. Although the peak at DTE 7 days reflects the immediate pricing of short-term event risks, the sustained rise in long-term IV reveals a deeper signal: investors believe that future macro uncertainty will be higher than historical average levels, rather than merely short-term emotional disturbances.

This poses a continuous challenge to the traditional 'shorting forward volatility' strategy, requiring extra caution.

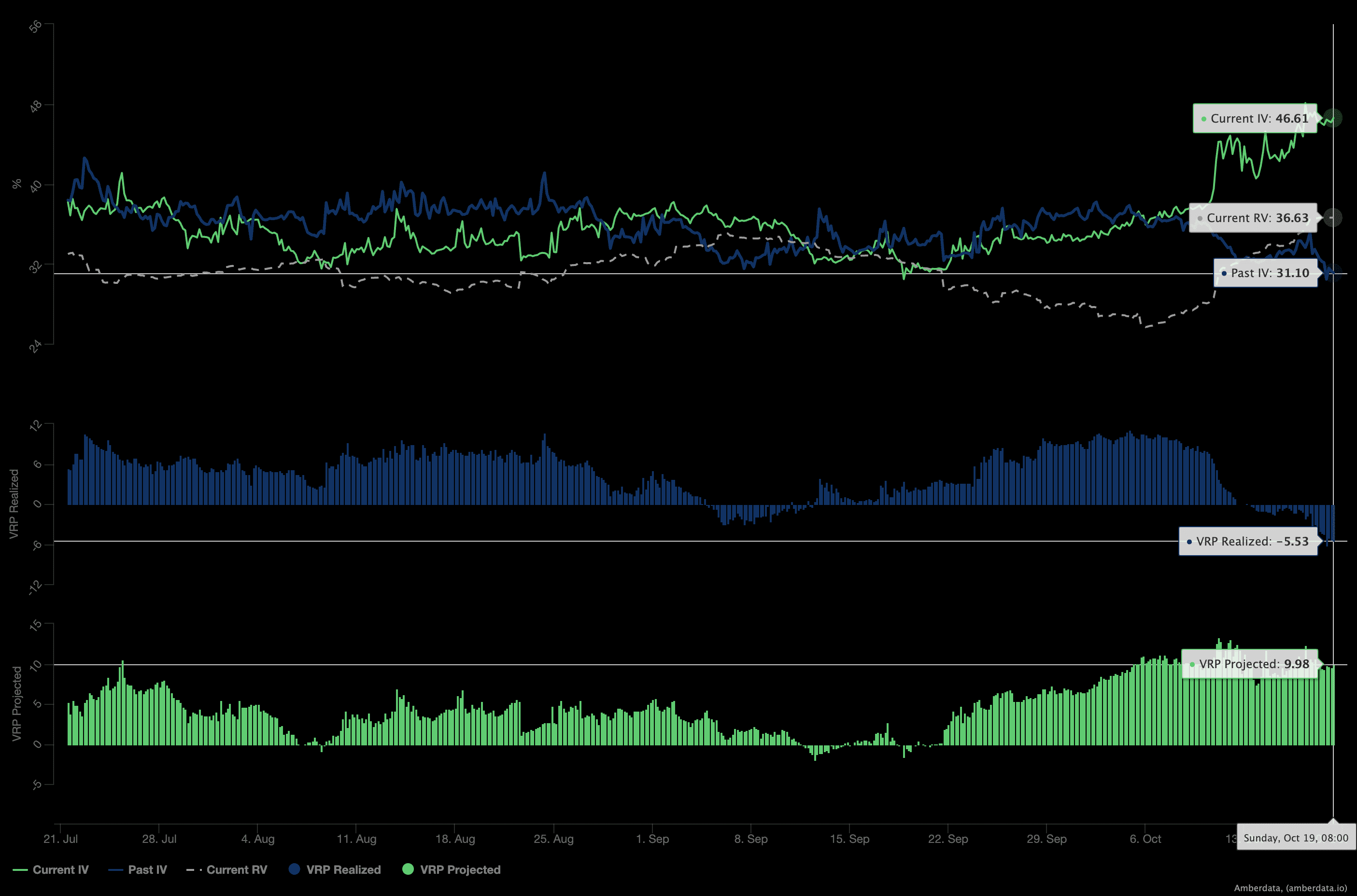

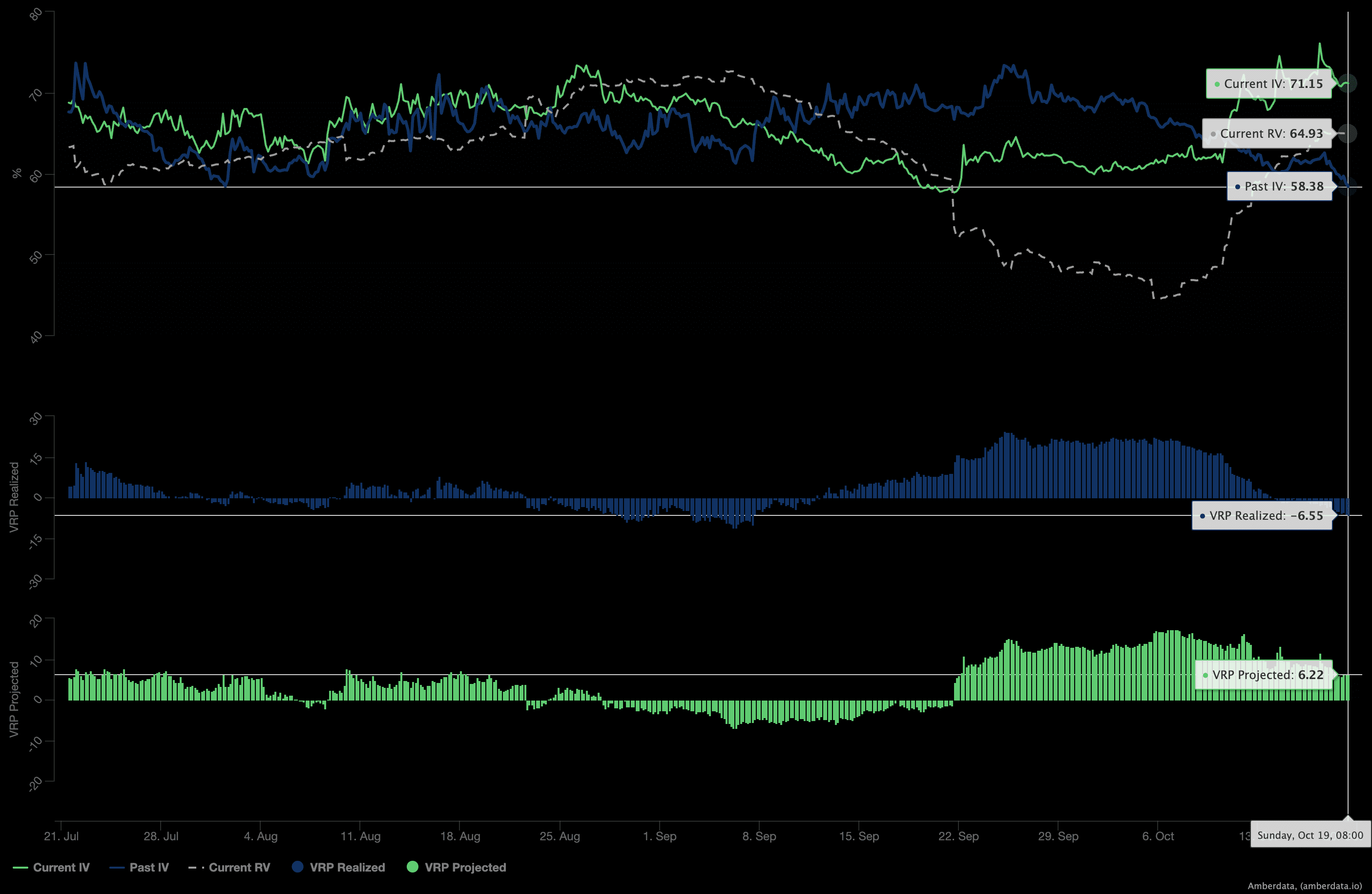

Volatility Risk Premium (VRP): Strategy warnings under contradictory signals

VRP (Volatility Risk Premium = Implied Volatility IV - Realized Volatility RV) is an important indicator for measuring whether option pricing is reasonable. Recent data presents a 'contradictory but important' dual signal:

VRP Realized (Realized Portion) is negative: this means that the actual volatility experienced in the market exceeds the expectations during option pricing (i.e., there have been extreme fluctuations that were not fully anticipated), which closely aligns with the characteristics of abrupt price jumps in the TACO market;

VRP Projected (Projected Portion) is at a high positive value (historical high): indicating that the current implied volatility (IV) is generally perceived by the market as 'overpriced', and it is expected that the actual volatility (RV) will significantly decline in the next 30 days—on the surface, this seems to suggest that the attractiveness of 'short volatility' strategies is increasing.

But must be cautious: given the recent negative VRP lesson (i.e., underestimating extreme volatility leading to risk exposure), blindly shorting volatility now requires extreme caution. A more prudent approach is to adopt strategies with a 'safety cushion' such as 'wide straddles', balancing potential returns and risks.

III. Option Strategy Recommendations: Synthetic Long Call—A tool for low-cost reversal positioning

Based on the characteristics of 'V-shaped reversals often occurring after panic sell-offs' in the TACO trading model, combined with the current 'VRP Realized being negative (market overly fearful) but VRP Projected being a high positive value (implied volatility being high)' contradictory pricing environment, we recommend a core strategy: Synthetic Long Call.

Strategy construction:

Buy one at-the-money (ATM) call option (Long Call), while selling one at-the-money Put (Short Put).

Core advantages:

Profit and loss structure close to spot long positions: the actual profit and loss curve of this combination is highly similar to directly buying the underlying spot, but cost optimization is achieved through the option combination;

Premium hedging cost: selling a Short Put can immediately generate premium income, which can directly cover part of the cost of buying a Long Call, thus positioning for a medium-term bullish trend at a lower net cost;

The anti-fragility of panic markets: when market panic selling leads to high IV (implied volatility), premium income can effectively hedge part of the risk; if the market continues to decline, investors only need to passively take delivery at the strike price of the Short Put, and the delivery cost is reduced due to the premium income—this is very suitable for those who are optimistic about mid-term price recovery and are willing to accumulate positions at low market levels.

In short, this is an efficient tool for 'counterattack' in the TACO market: betting on reversals at a lower cost while controlling downside risk through option structures.

IV. Disclaimer

This report is based on public market data and option theoretical models, aiming to provide investors with market information and professional analytical perspectives. All content is for reference and communication only and does not constitute any form of investment advice. Cryptocurrency and options trading are highly volatile and risky, which may lead to a total loss of capital. Before adopting any trading strategies, investors should fully understand the characteristics of option products, risk attributes, and their own risk tolerance, and must consult professional financial advisors. The analysts of this report are not responsible for any direct or indirect losses arising from the use of the content of this report. Past market performance does not predict future results; please make rational decisions.

Co-produced by: Sober Options Studio × Derive.XYZ