Sober Options Studio × Derive.XYZ Co-production

Written by Sober Options Studio analyst Jenna @Jenna_w5

1. The impact of interest rate cut expectations and the linkage with market pricing

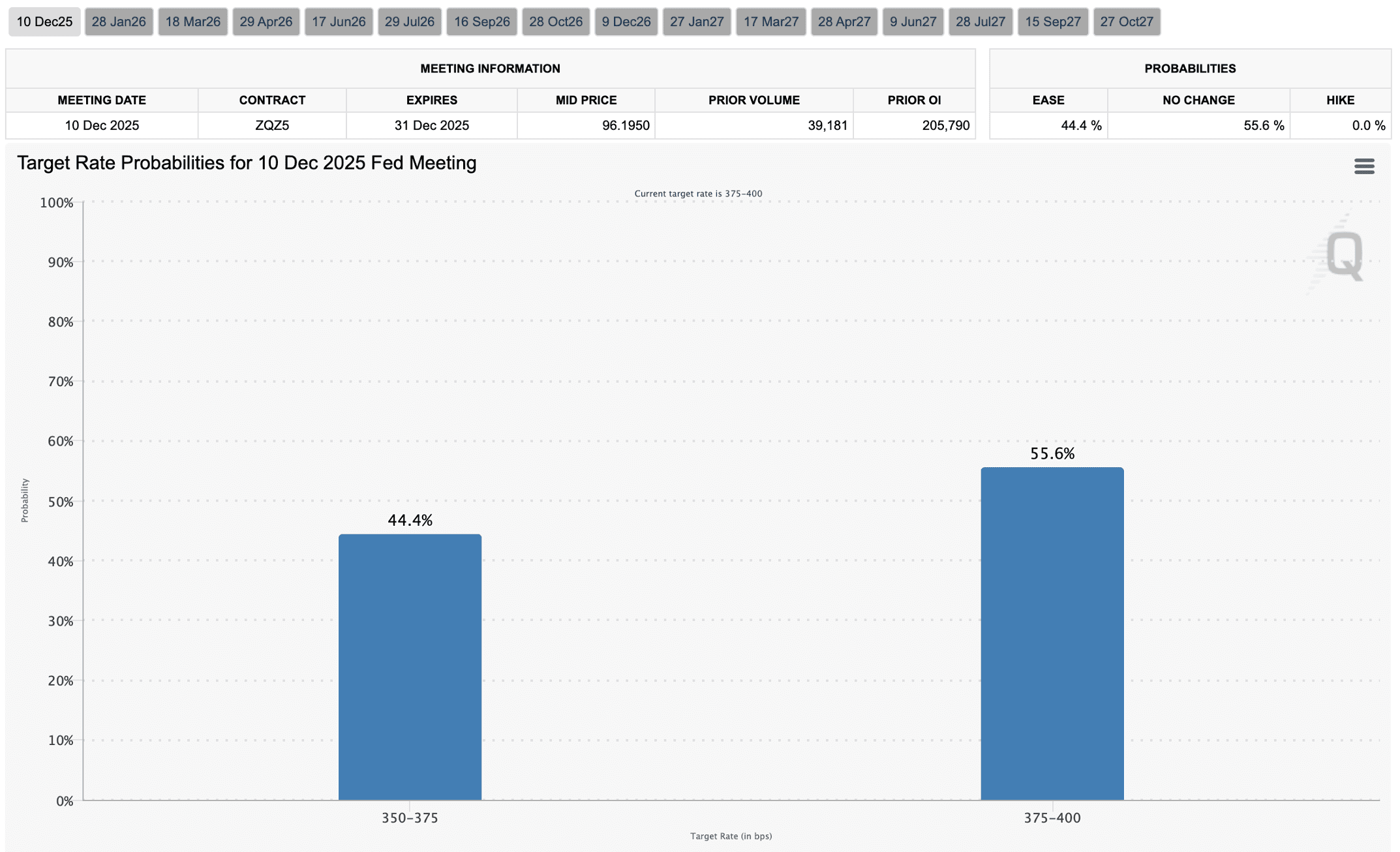

The core of last week's theme was the significant retreat in interest rate cut expectations that triggered a market correction. Last Saturday, both the Kansas City Fed and Dallas Fed released cautious signals regarding a rate cut in December at the annual energy conference, shifting the market from previous optimism about a year-end rate cut to a more cautious pricing. CME Group FedWatch shows that the probability of the third rate cut of the year on December 10 plummeted to about 44%, down approximately 20 percentage points from the previous week, with the market now leaning towards a trajectory of 'maintaining 2 rate cuts for the year, totaling 50bp.'

The effects of multi-dimensional reasons are showing.

First, structural pressure comes from tax and position adjustments at the U.S. level. On-chain analysis indicates that under the year-end tax optimization pressure, long-term holders (LTH) in the U.S. have shown selling signals throughout the cycle, and the selling pressure does not come from a single group but is released simultaneously from long-term holders of 6 months, 18 months, 3 years, and even 7 years. This phenomenon is highly correlated with the size of U.S. investors and the timing of tax settlement.

Second, market liquidity is marginally tightening. The government shutdown has led to a suspension of fiscal spending, with systemic funds being withdrawn in a scenario of fiscal surplus, combined with a cooling of optimistic sentiment regarding interest rate cuts, weakening risk appetite, and a general decline in the stock market, with related crypto assets and stocks facing pressure simultaneously.

Third, the interaction effect between the global funding environment and market sentiment is amplified. The decline in the probability of interest rate cuts in the short term leads to an increase in implied volatility and changes in skew in option pricing, prompting the market to price in higher risk premiums for mid-to-short-term volatility, further amplifying the price volatility of BTC/ETH.

In terms of price path, reviewing last week's market narrative, we can see the following transmission chain: decline in interest rate expectations → decline in risk appetite → tightening marginal liquidity → decrease in inflow of crypto-related cyclical funds → increased selling pressure on BTC/ETH → overall market pricing adjustment downward. Although liquidity may recover in the coming weeks, the dynamics of the U.S. market will remain the most direct driving factor in the short term, and the transmission effect on implied volatility (IV) in the options market and market sentiment will be particularly significant.

Last week’s main line was that macro uncertainty further penetrated into structural funds and tax factors, leading the market to recalibrate its expectations for the interest rate path at the end of the year. Risk appetite has significantly turned conservative, and the price volatility and downside pressure of BTC/ETH have risen in tandem, with the Skew and IV center in the options market also showing more pronounced defensive pricing signals.

2. BTC and ETH volatility structure analysis: short-term repricing and ongoing downside concerns

Recently, the volatility structure of BTC and ETH has shown that the short-term is pushed up due to the decline in interest rate expectations, while the medium-term risk premium remains high; Skew negative values are solidified, downside hedging demand converges; although VRP has overall converged, Realized still lags behind Projected, and market caution has not dissipated.

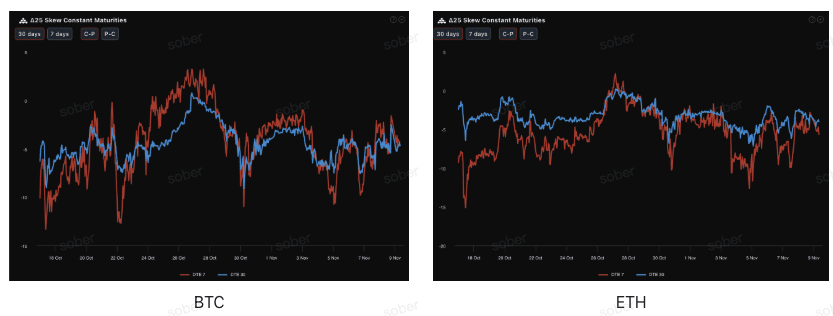

Skew: Negative value range solidified, but downside hedging demand shows a converging trend.

By observing the Delta 25 Skew (Call option implied volatility IV - Put option IV), the negative value of this indicator reflects the market's demand for hedging against downside tail risks. Currently, the Skew curves for both BTC and ETH remain in the negative range, but the magnitude of the negative value remains around -5, indicating that market concerns about downside risks persist. Compared to the previous week, the negative Skew values for ETH and BTC have begun to show a continuous convergence trend.

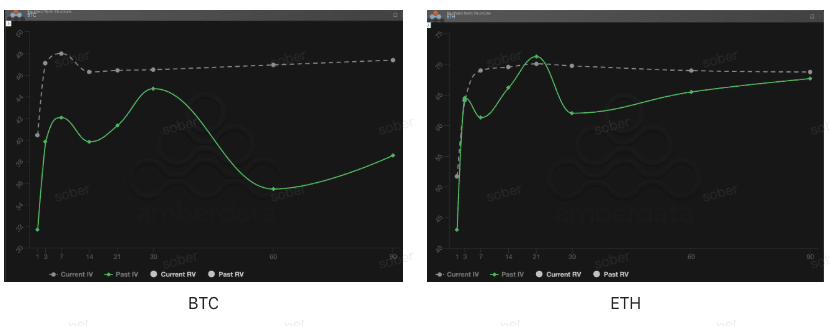

Term Structure: Short-term volatility is repriced upward, and medium-term risk premiums are still rising.

From the perspective of the term structure, last week's implied volatility curve for BTC and ETH did not show a typical Contango (near low, far high) pattern, but rather exhibited a significant rise in near-term IV with a high-level platform structure in the long term. The core driver of this change lies in the rapid recalibration of the probability of 'December rate cuts,' leading to a repricing of short-term event risks and causing short-term IV to turn upward.

Short-term IV rises (DTE 7–30 days): The near-term IV has shown a significant upward trend compared to the previous week, which is not due to new event shocks, but rather the market's rapid reaction to 'decline in interest rate expectations → rise in macro volatility' . Although Past IV has begun to decline, the re-elevation of Current IV indicates that short-term risk appetite has not improved and has instead entered a sensitive range.

Mid-to-long-term remains high (DTE 60/90 days): The mid-to-long-term IV is still consolidating at a high level and has not followed the short-term volatility decline, reflecting the market's clear pricing of systemic uncertainty (fiscal deadlock, Fed path, refinancing pressure, etc.) within 2–3 months.

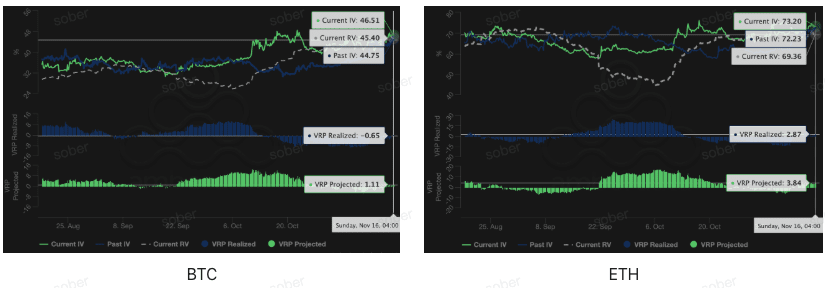

Volatility Risk Premium (VRP): Negative premium narrowing driven by rising implied volatility, risk remains high.

VRP (Volatility Risk Premium = Implied Volatility IV - Realized Volatility RV) is an important indicator to measure whether option pricing is reasonable. Currently, VRP is converging positively towards 0. The narrowing of VRP does not mean that risk appetite has recovered or that sellers have received adequate compensation; on the contrary, it reflects the market's consistent expectation of 'still high volatility in the future,' with option pricing adjusting towards a more conservative direction, and the risk exposure and hedging demand remain evident in the short term.

IV rise drives VRP narrowing: Investors have raised implied volatility based on expectations of mid-to-short-term uncertainties (macroeconomic policy, geopolitical or liquidity risks), thereby reducing the gap between IV and high RV, making VRP less negative or close to zero.

RV remains high: The realized volatility has not significantly declined, indicating that the actual volatility in the market in recent times remains significant, and the aftershocks of risk events are still being digested.

3. Options strategy recommendation: Bear Put Spread

Based on the current market structure dominated by deep negative Skew and the overall rising IV center, the core of the strategy should focus on limiting risks and preparing for possible moderate declines. In an environment where the market is generally bearish and liquidity is tightening, adopting a risk-limiting defensive strategy is the most prudent.

Core advantages: low cost, limited risk, making full use of the bearish premium brought by deep negative Skew, suitable for scenarios where the expected underlying asset will moderately decline or maintain a neutral bearish stance.

Strategy construction:

Buy one at-the-money or slightly out-of-the-money (ATM/Slightly OTM) put option (Long Put).

Sell one lower strike price put option with the same expiration date (Short Put).

Strategy goal: To collect premium by selling lower strike put options to reduce buying costs. This strategy aims to utilize the bearish premium brought by negative Skew to profit from moderate declines while limiting maximum losses to the net premium expenditure, which is far lower than the cost and risk of directly buying put options (Long Put).

Expiration date selection: Given the negative Skew and VRP Projected in the medium term (DTE 30/60 days) are more sticky, it is recommended to choose medium-term contracts with DTE 30 days or DTE 60 days to capture longer-lasting uncertainty premiums.

4. Disclaimer

This report is based on publicly available market data and options theoretical models, aiming to provide investors with market information and professional analytical perspectives. All content is for reference and communication only and does not constitute any form of investment advice. Cryptocurrency and options trading carry high volatility and risks, which may lead to a total loss of principal. Before adopting any trading strategy, investors should fully understand the characteristics of options products, risk attributes, and their own risk tolerance, and must consult professional financial advisors. The analysts of this report do not bear any responsibility for any direct or indirect losses arising from the use of the contents of this report. Past market performance does not indicate future results; please make rational decisions.

Jointly produced by: Sober Options Studio × Derive.XYZ