Sober Options Studio × Derive.XYZ Joint Production @DeriveXYZ_CN

Written by Sober Options Studio Analyst Jenna @Jenna_w5

1. Macro Black Holes and Platform Tightening: How does the market price 'Data Absence'?

Last week, the crypto asset market experienced a typical emotional correction, driven not by a single price event but by the dual overlap of macro systemic uncertainty and micro market deleveraging. As options traders, we must penetrate price fluctuations and understand the deeper logic of market risk pricing.

U.S. Government Shutdown: Creating a 'Data Black Hole' and Systemic Uncertainty

The U.S. federal government shutdown has entered its 38th day. The chain reaction of this event is causing concerns in the crypto market similar to those in traditional finance (TradFi) markets.

Reason and impact path of the event: The shutdown stems from the fundamental disagreements between the two parties in Congress over the new fiscal year's appropriations bill, centered on political polarization conflicts regarding healthcare benefits and government spending. For the market, its impact far exceeds the political stalemate itself, creating a 'data black hole':

Federal Reserve's data dilemma: Key economic data, including the U.S. October unadjusted CPI year-on-year, seasonally adjusted CPI month-on-month, and non-farm payroll report, cannot be released due to the shutdown of the Labor Department and the Commerce Department.

Impact path: This data is the cornerstone for the Federal Reserve's monetary policy formulation and market judgment of interest rate trends. The permanent absence or delay in data release has trapped the Federal Reserve in a 'data dilemma', exacerbating market uncertainty regarding future liquidity and interest rate environments. When decision-making and forecasting lose their anchor points, risk assets, especially highly volatile crypto assets, instinctively tend to retreat to hedge uncertainty premiums.

The market currently generally expects (Polymarket shows a 57% probability) that the shutdown will last until late November, which means macro uncertainty will be a persistent pricing factor.

Deribit's deleveraging: An accelerator of micro risks.

Just as macro risks are heating up, the major crypto options exchange Deribit has taken proactive risk control measures, further intensifying short-term pressure in the market:

Leverage reduction: Deribit announced a significant reduction in the futures leverage ratio for standard margin users from 50 times to 25 times.

Margin parameters raised: The platform also increased the price range variable for BTC, ETH, and sETH, with ETH's adjustment being more significant (from 14% to 18%).

Impact path:

Liquidity contraction: Reducing leverage and increasing margin essentially forces de-risking, reducing the scale of nominal positions in the market. For traders relying on high leverage for hedging or directional trading, this requires them to hold higher collateral or be forced to liquidate.

Amplifying short-term volatility: During market price corrections, these adjustments accelerate liquidations, amplifying short-term declines.

The shift in market sentiment last week was the result of macro uncertainty driving systemic risk, further amplified by the exchanges' deleveraging actions, leading to short-term corrections. All these factors will be clearly reflected in option pricing through implied volatility and skew structure.

II. Analysis of BTC and ETH volatility structure: Overall IV elevation and sustained downside concerns.

Last week's options structure indicates that the market is systematically pricing macro and liquidity risks. The core feature is no longer transient panic, but the entrenchment of deep bearish sentiment (sustained negative skew) and a comprehensive elevation of systemic risk premium (overall upward shift in term structure).

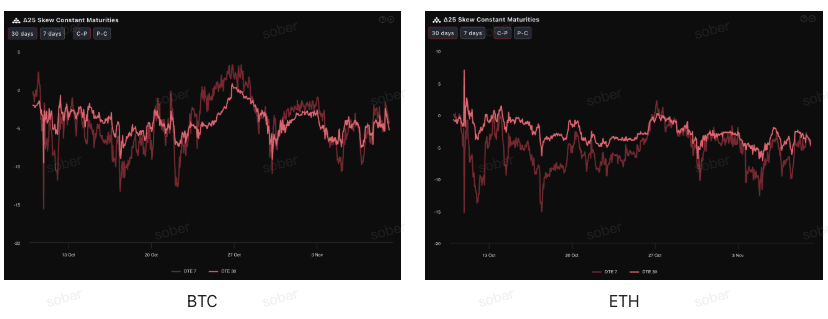

Skew: Deep negative values are entrenched, and mid-term put premiums are stickier.

By observing the Delta 25 Skew (implied volatility of call options - implied volatility of put options), the negative value magnitude reflects the market's demand for hedging against downside tail risk. Currently, both BTC and ETH's skew curves are in the negative range, but the negative value magnitude has increased again compared to last week (returning to around -5), indicating that the market's concern about downside risk is beginning to rise. From different assets' perspectives, compared to last week, ETH's negative skew value is starting to show a continuous convergence trend with BTC.

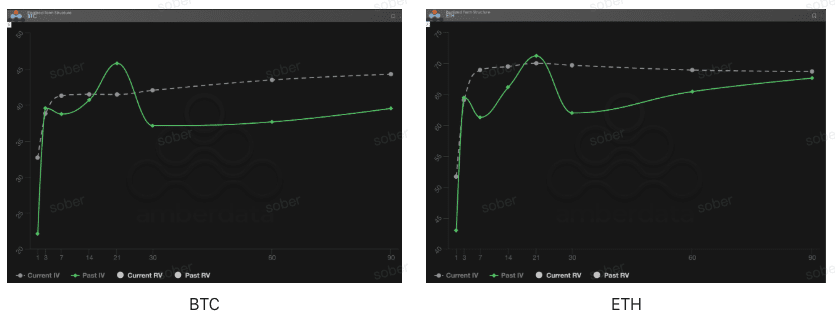

Term Structure: Elevated systemic risk premium.

From the perspective of term structure, the implied volatility curves of BTC and ETH maintain a significant contango (near low, far high) pattern, but the underlying pricing logic is shifting from 'short-end event digestion' to 'mid-term systemic risk elevation'. In other words, although short-term shocks are easing, the overall risk premium has not declined; instead, it has concentrated on the mid to long end.

Short-term IV decline: Whether BTC or ETH, the near-end (DTE 7–30 days) Current IV has declined compared to previous event highs, but this decline more reflects the clearance of short-term event shocks rather than a repair of risk appetite. Compared to Past IV, the decline in short-end volatility has not led to a downward shift in the entire curve, indicating that the market's concern about systemic risk has merely shifted from 'immediate shocks' to 'structural factors'.

Long-end IV rise: The long-end (DTE 60/90 days) IV remains at a high level, and the market's pricing for mid-term (2-3 months) systemic uncertainty (such as the prolonged government shutdown and the Federal Reserve's rate-cutting process) has not relaxed.

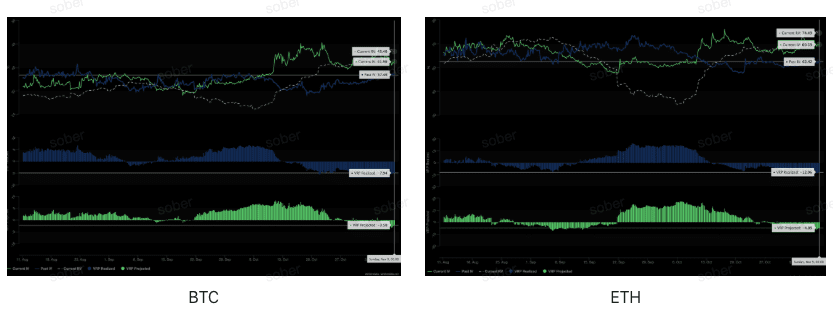

Volatility risk premium (VRP): Negative premium further deepens, and the market feels more pressure.

VRP (Volatility Risk Premium = Implied Volatility IV - Realized Volatility RV) is an important indicator for measuring whether options pricing is reasonable. Currently, in an environment where VRP Realized continues to be deeply negative, the value of VRP Projected has remained negative after turning from positive last week, indicating that the market has learned from experiences of 'underestimating extreme volatility' and is taking a cautious attitude towards future volatility.

VRP Projected negative value expands: The volatility expectation for the next 30 days has been further revised upward, and investors' pricing tends to be more conservative against potential disruptions.

VRP Realized negative value deepens: The actual volatility over the past 30 days remains high, leading to an expansion of the deviation between implied and realized volatility, reflecting that the market's absorption of recent volatility shocks is still inadequate.

III. Recommended Options Strategy: Bear Put Spread

Based on the current market structure dominated by deep negative skew and overall elevated IV center, the core of the strategy should focus on limiting risk and preparing for potential moderate declines. In an environment where the market is generally bearish and liquidity is tightening, adopting a risk-limiting defensive strategy is the most prudent.

Core advantage: Lower cost, limited risk, fully utilizing the put premium brought by deep negative skew, applicable to scenarios where the underlying asset is expected to decline moderately or maintain a neutral bearish stance.

Strategy construction:

Buy one at-the-money or slightly out-of-the-money (ATM/Slightly OTM) put option (Long Put).

Sell one put option with a lower strike price and the same expiration date (Short Put).

Strategy objective: Capture premium by selling put options with lower strike prices to reduce buying costs. This strategy aims to take advantage of the put premium brought by negative skew, profiting from moderate declines while limiting maximum losses within the net premium expenditure, far below the cost and risk of directly buying put options (Long Put).

Expiration date selection: Given the negative skew and VRP Projected being stickier in the mid-term (DTE 30/60 days), it is recommended to select mid-term contracts with DTE 30 days or DTE 60 days to capture longer-lasting uncertainty premiums.

IV. Disclaimer

This report is based on publicly available market data and options theoretical models and aims to provide investors with market information and professional analytical perspectives. All content is for reference and communication purposes only and does not constitute any form of investment advice. Cryptocurrency and options trading carry high volatility and risk, which may lead to the total loss of principal. Before adopting any trading strategy, investors should fully understand the characteristics of options products, risk attributes, and their own risk tolerance, and must consult professional financial advisors. The analysts of this report bear no responsibility for any direct or indirect losses arising from the use of this report's content. Past market performance does not predict future results; please make rational decisions.

Co-produced by: Sober Options Studio × Derive.XYZ