Sober Options Studio × Derive.XYZ Joint Production @DeriveXYZ_CN

Written by Sober Options Studio Analyst Jenna @Jenna_w5

1. Macro Insight: The Data Vacuum and the Prisoner's Dilemma of Policy Games

Last week, the crypto market fell into a strange state of 'divergence'. Although CME data showed a significant rebound in the probability of a rate cut in December, the prices of BTC and ETH did not rebound and instead showed signs of fatigue after a decline. On a macro level, the government shutdown crisis has led to a halt in data releases, casting a thick layer of 'data fog' over the Federal Reserve's decision-making. The options market is re-pricing for this 'unknown' uncertainty: IV (Implied Volatility) on the short end has significantly increased, Skew is deeply negative and solidified, and the market is shifting from merely 'trading rate cuts' to 'trading recession and policy error risks'.

'Data fog' leads to a reconstruction of pricing logic

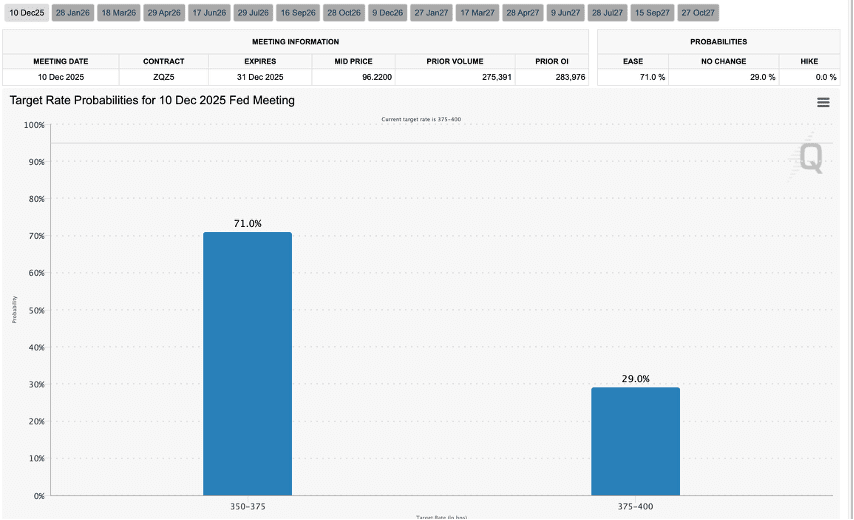

According to the latest calendar, the originally critical October CPI report has been canceled due to government funding interruptions, and the November CPI data announced on December 18 will be released later than the Fed's interest rate meeting. This means that the Fed will make a rate decision in December in the absence of key inflation data (Blind Flying).

This kind of 'information vacuum' is deadly for risk assets. Even though CME FedWatch shows that the probability of a rate cut in December has risen to 71% (the market bets on a total rate cut of 75bps this year), asset prices have not followed suit. The reason is that the market is concerned that in the absence of data support, the Fed's rate cut may be seen as a 'panic measure' rather than a 'preventive measure', or that the Fed may choose to pause rate cuts due to a lack of data, leading to policy errors. What the market dislikes is not bad news, but uncertainty. The current 'second-order uncertainty due to lack of data' makes funds more inclined to wait on the sidelines rather than entering the fray.

The swings in rate cut expectations and liquidity trap

The previously expected 25bps rate cut in October was met, but the subsequent delay in non-farm data release and the absence of CPI interrupted the originally smooth 'soft landing' trading narrative. Although the probability of a rate cut has rebounded, market confidence has not. What we see is a typical bearish divergence: rate cut expectations are rising, but prices are falling. This indicates that the market is pricing in a deeper risk—that the pace of economic slowdown may outstrip the pace of Fed rate cuts (Behind the Curve).

Second, deep analysis of BTC & ETH options market data

Combining the chart data provided by Derive.XYZ, the options market is using high premiums to hedge this 'unknowable' risk.

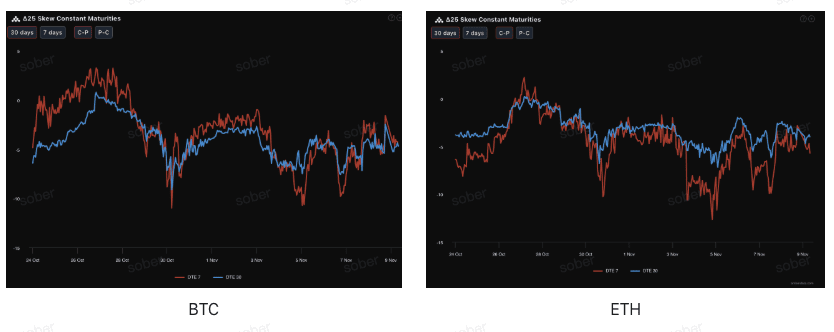

Skew: bearish sentiment solidified, short-term panic intensified

By observing Delta 25 Skew (implied volatility IV of call options - IV of put options), the negative value range reflects the market's hedging demand for downside tail risks.

Normalization of deep negative values: Both curves have fallen below -5%. This means that demand for puts (put options) is extremely strong, and traders are willing to pay extremely high premiums for downside protection. This ongoing negative skew indicates that bearish forces currently completely dominate pricing power.

Inverted signal in the term structure: Notably, the volatility range of DTE 7 (deep red line) is much greater than that of DTE 30, and at certain moments it is more 'negative' than the long term. This sharp decline in short-end skew is usually a direct reflection of panic selling in the spot market.

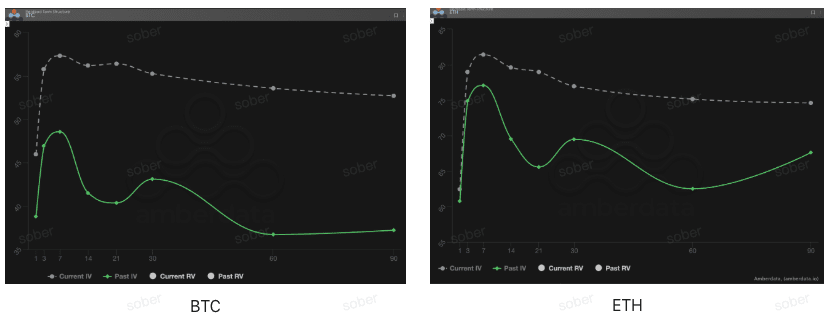

Term Structure: atypical contango appears, near-end hedging sentiment explodes

From the perspective of the term structure, last week's implied volatility curves for BTC and ETH were not in the typical contango (near low far high) shape, but showed a significant lift in near-term IV, maintaining a high level at the far end, forming a 'hump' structure.

Curve shape anomaly: A normal term structure should be contango (left low right high, near IV lower than far IV). However, the current gray dashed line (Current IV) shows a sharp rise in the near end (DTE 1-7), forming a distinct 'hump'.

Event-driven IV surge: Current IV is significantly higher than Past IV (green solid line) at the short end. This is not a normal market condition but a typical 'event hedging' mode. The market is frantically buying short-term options before and after the December interest rate meeting, which has significantly pushed up the near-end IV. This structure typically appears before major uncertainty events (such as elections or the current 'data blind box' interest rate meeting).

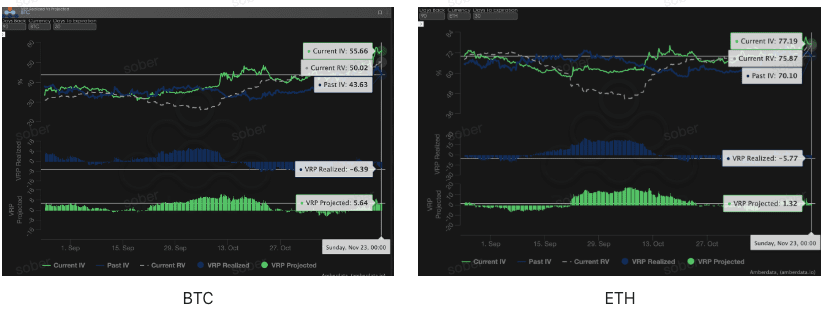

Volatility Risk Premium (VRP): 'Revenge' return of realized volatility

VRP (Volatility Risk Premium = Implied Volatility IV - Realized Volatility RV) is an important indicator for measuring whether options pricing is reasonable. The current market is in a state of intense correction characterized by 'unsettled shock'. Although IV has risen significantly to correct pricing deviations, the structural divergence in VRP data reveals potential risks: historical actual volatility far exceeds expectations, and the current high premium may seem enticing but may still be insufficient to cover future tail risks.

Realized VRP (Realized) deep negative warning: Both BTC and ETH's realized VRP are in the deep negative zone, indicating that the actual volatility (RV) over the past 30 days has greatly exceeded the implied volatility (IV). Option sellers have just experienced a severe blow from 'underestimating extreme volatility', and the market's vulnerability is extremely high; any sudden news could trigger a gap.

Projected VRP positive value trap: Although the projected VRP has risen to a positive value, indicating that IV is relatively overestimated, blindly shorting volatility (Short Volatility) is extremely dangerous before the realized deep negative has not been repaired. Investors should avoid naked selling and instead adopt spread strategies, earning high IV premiums while strictly locking in downside tail risk.

Three, options strategy recommendation: Bear Put Spread

Based on the above analysis: short-term IV is extremely high (options are expensive), skew is deeply negative (puts are more expensive), projected VRP is positive (suitable for seller logic). Although we believe that the long-term rate cut cycle remains unchanged, there are short-term risks of 'data fog' and a pause in rate cuts, making blind bottom fishing extremely risky. The strategy should focus on being 'bearish but hedging Vega risk'.

Core advantage: low cost, limited risk, fully utilize the put premium brought by deep negative skew, suitable for scenarios where the expected underlying asset will decline moderately or maintain a neutral bearish stance.

Strategy construction:

Buy a slightly in-the-money or out-of-the-money (ATM/Slightly OTM) put option (Long Put).

Sell a put option with a lower strike price and the same expiration date (Short Put).

Strategy objective: To collect premiums by selling put options with lower strike prices, thus reducing the cost of buying. This strategy aims to take advantage of the put premium brought by negative skew, profiting from moderate declines while limiting maximum losses within the net premium expenditure, far below the cost and risk of directly buying put options (Long Put).

Expiration date selection: Given the negative skew and VRP projected for the medium term (DTE 30/60 days) are more sticky, it is recommended to choose medium-term contracts with DTE 30 days or DTE 60 days to capture longer-lasting uncertainty premiums.

Four, Disclaimer

This report is based on publicly available market data and options theoretical models and aims to provide investors with market information and professional analytical perspectives. All content is for reference and communication only and does not constitute any form of investment advice. Cryptocurrency and options trading involves high volatility and risk, which may lead to the total loss of principal. Before taking any trading strategy, investors should fully understand the characteristics of options products, risk attributes, and their own risk tolerance, and must consult professional financial advisors. The analysts of this report are not responsible for any direct or indirect losses arising from the use of this report's content. Past market performance does not predict future results; please make rational decisions.

Jointly produced by: Sober Options Studio × Derive.XYZ