Sober Options Studio × Derive.XYZ Joint Production

Written by Sober Options Studio Analyst Jenna

1. The impact of stablecoin trading hitting new highs on the crypto market

This week, the stablecoin market has reached a historic breakthrough: its monthly trading volume (primarily referring to real-world scenario transactions for goods, services, and transfers) has set a new record, surpassing $10 billion, significantly higher than February's $6 billion. This milestone event marks a solid step towards transforming crypto assets from mere speculative tools into global payment and business solutions, and has profound implications for the long-term value narrative of underlying assets like BTC and ETH.

The surge in stablecoin trading volume is not coincidental; it is driven by two core factors:

Regulatory Certainty: The key time point is after the signing and implementation of the Genius Act in the United States. The regulatory framework for the issuance and use of stablecoins is gradually becoming clear, greatly reducing the compliance risks for institutions and enterprises adopting stablecoins. Regulation has shifted from a 'sword of Damocles' to a 'guiding light,' opening the door to large-scale commercial applications.

Enterprise Efficiency Driven: The report shows that B2B transfers currently account for about two-thirds of the total stablecoin payment volume. This reflects that enterprises are actively using stablecoins to avoid the high costs and long delays commonly found in traditional international bank transfers. For corporate payments averaging around $250,000, the instant settlement capability provided by stablecoins is disruptively attractive.

The expansion of stablecoin payment scale is having a structural and long-term impact on the crypto options market and the entire crypto ecosystem. Its impact path can be summarized as follows: the growth in stablecoin payment volume increases the real demand for underlying blockchain networks (such as Ethereum, Solana, etc.), thereby locking in more liquidity in the long term. This accumulation of liquidity helps reduce the extreme vulnerability of the market, making the value foundation of the entire crypto system more solid.

In this process, the positioning of BTC and ETH is also continuously evolving. The widespread use of stablecoins fundamentally strengthens the narrative of 'value capture' for crypto assets. As the primary stablecoin issuance and trading platform, Ethereum's Gas Fee (transaction fees) demand will continue to rise, directly boosting its network value. Bitcoin, on the other hand, has become the most reliable reserve asset in the new crypto financial system due to its characteristics of 'digital gold' and 'store of value.' Therefore, the intrinsic value of long-term bullish options on Bitcoin will further increase.

From the perspective of volatility structure, as the ecosystem of stablecoins matures and becomes widespread, the daily volatility of the crypto market may gradually decrease, but the impact of 'black swan' events will also weaken simultaneously. Overall, the market is moving towards a stage where volatility is more controllable and the structure is more robust, which will bring higher certainty and efficiency to options market pricing.

II. Analysis of BTC and ETH Volatility Structure: The market is shifting from 'hedging' to 'structural optimism.'

This week's options data shows that the market is digesting the positive fundamentals brought by stablecoin expansion and other macro benefits, with overall sentiment significantly easing from last week's panic hedging, showing a pricing tendency of optimism for the long term. Short-term volatility pressure has been significantly released, and the market focus is shifting from 'hedging' to 'structural optimism.'

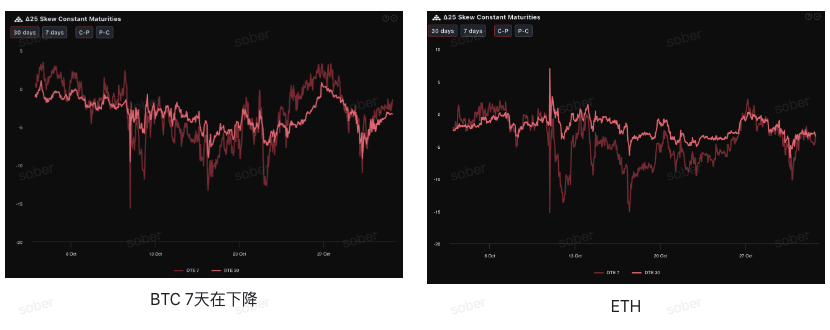

Skew: ETH's short-term bullish sentiment recovers faster.

Observing the Delta 25 Skew (implied volatility IV of call options - IV of put options), the negative amplitude of this indicator reflects the market's hedging demand against downside tail risks. Currently, the Skew curves of BTC and ETH are both in the negative range, but the negative amplitude has slightly narrowed, indicating that the market's concern about downside risk continues to diminish.

From the perspective of different assets, compared to last week, the negative Skew of ETH is beginning to converge with BTC, and the DTE 7-day negative Skew of ETH is similar to its DTE 30-day, indicating a warming market confidence in ETH.

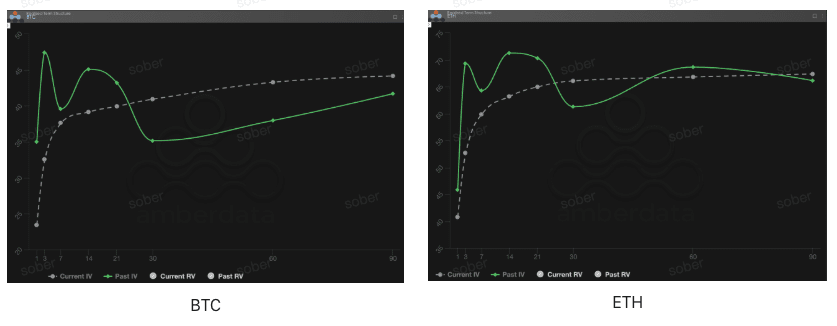

Term Structure: Near-term IV falls, while long-term volatility center remains strong.

From the perspective of term structure, the implied volatility curves of BTC and ETH maintain a clear Contango (near low, far high) shape, indicating that the short-term risk premium is decreasing, while the long-term contracts maintain relatively stable expectations. The near-term IV has significantly fallen compared to the previous 'event peak,' indicating that the short-term volatility driving force in the market is weakening.

Short-term IV falls: Whether for BTC or ETH, the current Current IV (implied volatility) curve is lower compared to the historical Past IV (implied volatility) during the near term (DTE 7-30 days). This is corroborated by the repair of the Skew, suggesting that the immediate impact of short-term macro risks seems to have been partially digested, and the premium for short-term event risks is decreasing.

Long-term IV remains strong: The long-term (DTE 60/90 days) IV remains at a high level, indicating that the market has not relaxed its pricing of systemic uncertainties (such as prolonged government shutdowns and the Federal Reserve's interest rate cut process) in the medium term (2-3 months).

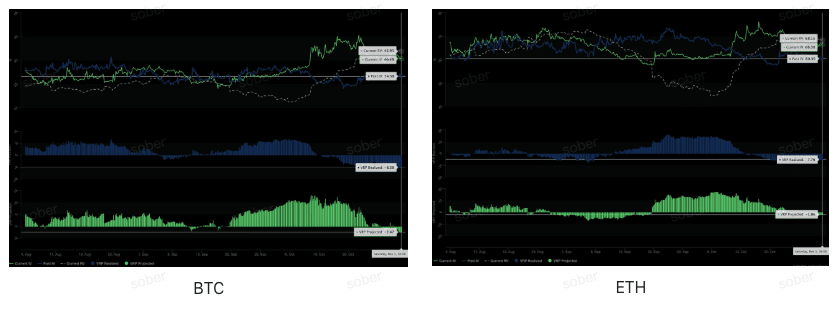

Volatility Risk Premium (VRP): BTC's volatility surprises and expectations are more extreme.

VRP (Volatility Risk Premium = Implied Volatility IV - Realized Volatility RV) is an important indicator for measuring whether options pricing is reasonable. Currently, in an environment where VRP Realized remains deeply negative, the value of VRP Projected has shifted from positive to negative, indicating that the market has experienced and learned from the lessons of 'underestimating extreme volatility' and is taking a cautious attitude towards future volatility.

It is worth mentioning that BTC's volatility surprises and future volatility expectations are significantly higher than those of ETH, showing stronger sensitivity to market sentiment and volatility elasticity; while ETH's volatility structure is more robust, with faster short-term repair speed, but a more moderate long-term premium.

BTC's VRP Realized (-8.38) is deeper in negative value than ETH's (-7.76), indicating that the actual volatility (RV) experienced by BTC in the past 30 days exceeded the market's original options pricing expectations, and the market's underestimation of its volatility is more significant.

At the same time, BTC's VRP Projected (-2.47) is also significantly lower than ETH's (-1.86), indicating that the market's expectation of BTC's volatility over the next 30 days is more inclined towards the upside, meaning investors believe that BTC's future volatility may still exceed the current implied level.

III. Recommended Options Strategy: Construct a Bull Call Spread.

Combining the positive fundamentals brought by stablecoins and the signals of term structure returning to Contango, we judge that the market's mid-term trend leans towards a stable bullish outlook. We recommend relatively risk-controlled and clearly profitable bullish strategies: Bull Call Spread. This strategy aims to leverage mid-term bullish sentiment while partially hedging the cost of buying low-priced call options by selling high-priced call options.

Strategy Construction

Buy one call option with a lower strike price (DTE 30 days or DTE 60 days).

Sell one call option with the same expiration date but a higher strike price.

Core Advantages and Risks

High cost efficiency: By selling high strike price Call Options to collect premiums, it can effectively reduce the net premium outlay of the entire portfolio, significantly improving the efficiency of capital utilization.

Controllable risk and return: It structurally predefines the profit and loss range: when the underlying price exceeds the high strike price, the profit is capped; when the price is below the low strike price, the loss is limited to the initial net premium outlay. The maximum risk and potential return can be clearly defined at the time of establishing the position, thus achieving a stable and predictable return structure.

IV. Disclaimer

This report is based on public market data and options theoretical models, aiming to provide investors with market information and professional analytical perspectives. All content is for reference and communication purposes only and does not constitute any form of investment advice. Cryptocurrency and options trading carry a high degree of volatility and risk, which may lead to a total loss of principal. Before adopting any trading strategy, investors should fully understand the characteristics and risk attributes of options products and their own risk tolerance, and must consult professional financial advisors. The analysts of this report are not responsible for any direct or indirect losses resulting from the use of this report's content. Past market performance does not indicate future results; please make rational decisions.

Co-produced by: Sober Options Studio × Derive.XYZ