The key economic data for the U.S. for October and November, postponed due to the government shutdown, will be intensively released this week, becoming the last and largest source of uncertainty for the financial markets at the end of the year.

Due to the previous U.S. government shutdown, the core economic data such as non-farm employment and CPI for October and November, originally scheduled for release in early November, have been postponed to this week for concentrated issuance. This means that the usually calm period in mid to late December will rarely welcome a 'data bomb' that can reshape market logic.

Market analysis generally views this week as the core window period for determining the asset trends at the beginning of 2026. The postponed 'terrifying data' retail sales will also be released, further increasing market volatility.

I. An Unconventional Data Release Week

I. An Unconventional Data Release Week

The core logic of global market trading this week revolves entirely around a special event: the combined release of U.S. core economic data for October and November.

● Due to the previous U.S. government shutdown, several key data releases, including non-farm employment, CPI, and retail sales, have been forced to be delayed. The U.S. Department of Labor is scheduled to release a combined non-farm employment report for October and November on this Tuesday (December 16).

● Similarly, the delayed CPI data for October and November is scheduled to be released this Thursday (December 18). This unconventional and high-density data release disrupts the market's original seasonal calm rhythm, making mid-December a decisive moment for the direction of asset prices at the end of the year and even at the beginning of next year.

● The importance of data lies in the 'employment-inflation' picture it paints, which is the cornerstone of the Federal Reserve's interest rate decisions.

II. Market Expectations: A Contradictory Answer Sheet

Before the data is released, the market has already formed a contradictory 'expected answer sheet' through surveys conducted by agencies such as the Wall Street Journal.

Data Category

Release Time

Data Cycle

Market Forecast Value

Non-Farm Employment Population

December 16 (Tuesday)

November

+50,000

Unemployment Rate

December 16 (Tuesday)

November

4.50%

CPI Year-on-Year Rate

December 18 (Thursday)

November

3.10%

Core CPI Year-on-Year Rate

December 18 (Thursday)

November

3.00%

● The market expectation itself reveals the core contradictions of the current economy: on one hand, the market expects employment growth to slow significantly (with the November non-farm expectation at only +50,000), indicating that the economy may be cooling.

● On the other hand, inflation expectations stubbornly remain high (CPI expectation 3.1%, core CPI expectation 3.0%), far above the Federal Reserve's 2% target, showing that the anti-inflation process is stuck. This contradictory answer sheet is a microcosm of the Federal Reserve's decision-making dilemma and the source of market volatility.

III. The Federal Reserve's Dilemma: Finding Balance Amid Contradictory Data

No matter what combination of data emerges, it will put the Federal Reserve, which follows a 'data-dependent' model, into a deeper dilemma.

● If the data combination is 'Weak Employment + High Inflation', the so-called signs of 'stagflation', this would be the worst-case scenario. The Federal Reserve would have to make a painful choice between supporting economic growth and curbing inflation, and policy uncertainty would reach its peak.

● If the data combination is 'Strong Employment + High Inflation', this will confirm some Federal Reserve officials' concerns that the risk of an overheating economy has not been eliminated and that inflation is entrenched. The market's expectations for the Federal Reserve to maintain high interest rates 'higher for longer' will be reinforced, and the possibility of restarting discussions on interest rate hikes cannot be ruled out.

● The only combination that could relieve the market is 'Weak Employment + Low Inflation'. This scenario would clearly point to economic cooling and controlled inflation, paving the way for the Federal Reserve to initiate a clear rate cut cycle in 2026. However, given the current inflation stickiness, the probability of this scenario occurring is relatively low.

IV. Asset Prices Face a 'Stress Test'

This delayed data 'make-up exam' will conduct a comprehensive 'stress test' on major global asset classes.

● Foreign Exchange Market: The dollar index will face a direct test. Any data indicating the relative resilience of the U.S. economy or stubborn inflation may push the dollar stronger. Conversely, if the data is broadly weak, the dollar will come under pressure.

● Stock Market: The U.S. stock market, especially interest rate-sensitive tech growth stocks, will face huge volatility. Stronger-than-expected data may undermine hopes for interest rate cuts, leading to a stock market correction; weaker-than-expected data may trigger concerns about economic recession, also unfavorable for the stock market.

● Bond Market: U.S. Treasury yields, especially short-term yields, will be most sensitive to inflation data. Higher-than-expected CPI data may trigger a sell-off in Treasury bonds, pushing up yields.

● Gold: Gold prices will face a dilemma. High inflation data theoretically benefits gold as an anti-inflation asset, but it will also raise the dollar and interest rates, putting pressure on gold. The trend of gold will depend on whether the market leans more towards trading the 'inflation' logic or the 'interest rate' logic.

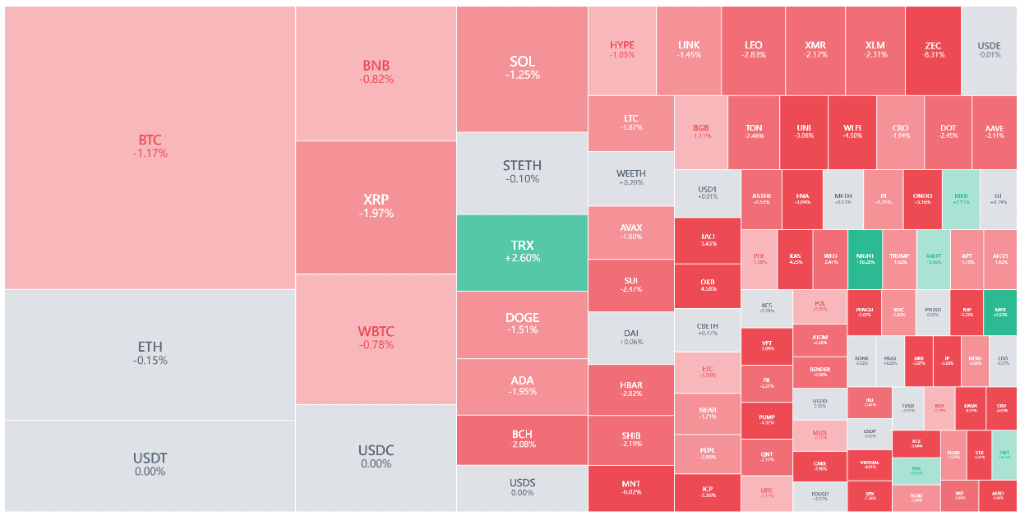

V. Cryptocurrency Market: Standing at the Crossroads of Liquidity

V. Cryptocurrency Market: Standing at the Crossroads of Liquidity

As a 'high-sensitivity detector' of global liquidity and risk appetite, the cryptocurrency market is at a crucial crossroads.

● Traditional macro logic still dominates the short-term trend in the cryptocurrency market: expectations of loose liquidity act as a booster, while expectations of tightening act as a fire extinguisher. Therefore, this week’s data will directly influence the prices of mainstream cryptocurrencies like Bitcoin by affecting expectations for Federal Reserve policy.

Scenario 1: Data Strengthens Tightening Expectations (High Probability)

If any of the non-farm or CPI data is significantly stronger than expected, market bets on rate cuts in 2026 will significantly retreat. This will lead to:

1. Expectations of marginal tightening in dollar liquidity are heating up.

2. Market risk appetite is suppressed.

In this scenario, cryptocurrencies, as pioneering risk assets, are likely to face sell-offs alongside traditional U.S. stocks, with volatility sharply amplified.

Scenario 2: Data Strengthens Rate Cut Expectations (Low Probability)

If the data shows a significant cooling in the job market and a notable decline in inflation, the market will reignite hopes for an early pivot from the Federal Reserve. This would provide an ideal macro environment for the cryptocurrency market: a weaker dollar, declining real interest rate expectations, and a return of risk appetite. Bitcoin is expected to lead a rebound in risk assets.

Considering the stubbornness of inflation, the likelihood of the first scenario occurring is higher. Participants in the cryptocurrency market must prepare for potential 'tightening shocks' and closely monitor the immediate reactions of the dollar index (DXY) and the U.S. 2-year Treasury yield, which are usually more accurate leading indicators of capital flow.

"All eyes are on the upcoming U.S. employment and inflation data." Traders are holding their breath, as this overdue data storm will directly conclude 2025 and set the tone for investments in 2026.

Whether in the foreign exchange, stock market, or cryptocurrency world, after this week, a clearer macro trading map for 2026 will be drawn.

Join our community to discuss and grow stronger together!

Official Telegram Community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX Benefit Group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance Benefit Group: https://aicoin.com/link/chat?cid=ynr7d1P6Z