The current market phase can be characterized as a range-bound consolidation following a high-level correction, with momentum conditionally tilted to the downside. Over the past three months, gold and silver have continued to rise, while Bitcoin has remained largely sideways. This divergence reflects increased demand for traditional safe assets amid geopolitical and policy uncertainty, expectations of lower real interest rates, and the structural ease with which institutional capital allocates to precious metals. Silver has further amplified gold’s move due to tighter supply conditions and higher sensitivity to speculative flows.

Bitcoin has not followed this move because it is still treated primarily as a high-beta risk asset, rather than a pure safe haven. In risk-off environments, capital tends to flow first into gold and government bonds, while Bitcoin is often a secondary consideration. Unlike gold’s long-term, less price-sensitive buyer base, Bitcoin remains more exposed to short-term positioning and marginal demand, making macro tailwinds alone insufficient to sustain an uptrend.

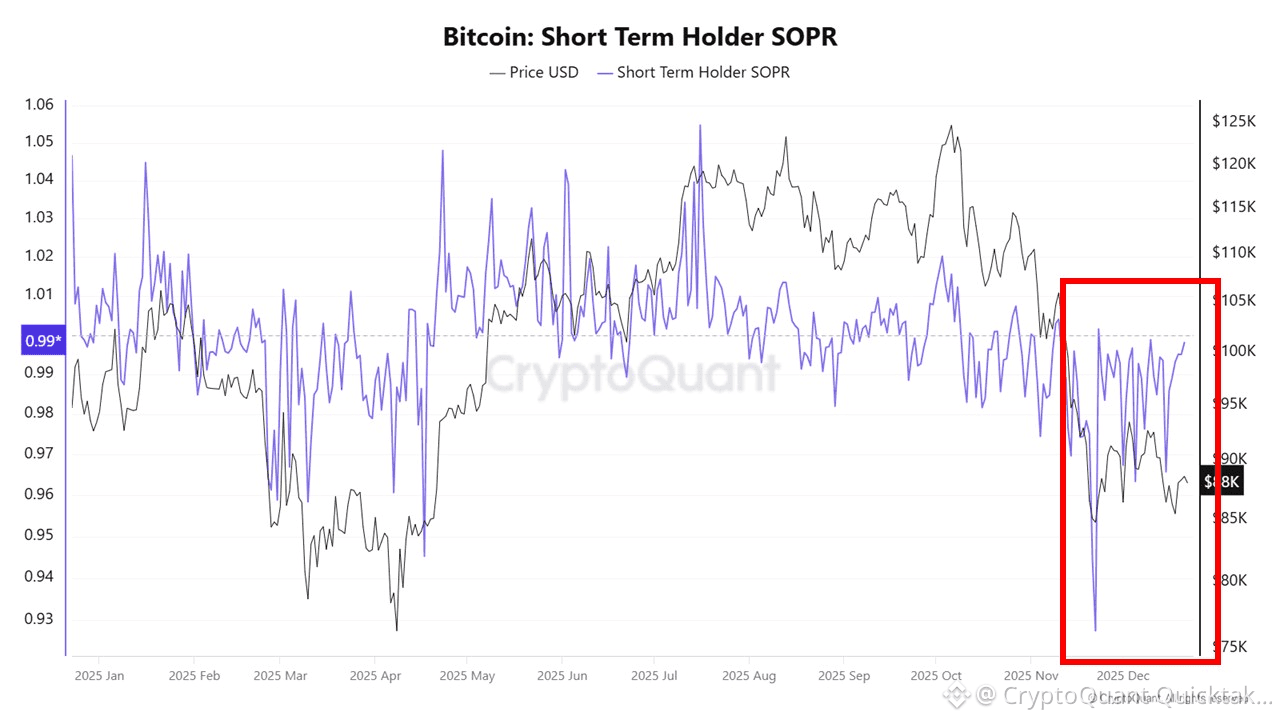

CryptoQuant data supports this view. Bitcoin apparent demand has recently turned negative, indicating that new demand is not expanding despite prices holding at elevated levels. In parallel, Short-Term Holder SOPR has spent more time below 1, suggesting that short-term holders are exiting at a loss or near breakeven, increasing selling pressure on rebounds. As long as capital favors gold and silver, Bitcoin’s internal demand structure remains a limiting factor.

The base scenario is that gold and silver stay supported by safe-asset flows, while Bitcoin’s upside remains capped by weak demand and short-term holder pressure. However, if apparent demand turns sustainably positive and STH SOPR stabilizes above 1, this assessment would need to be reconsidered.

Written by XWIN Research Japan