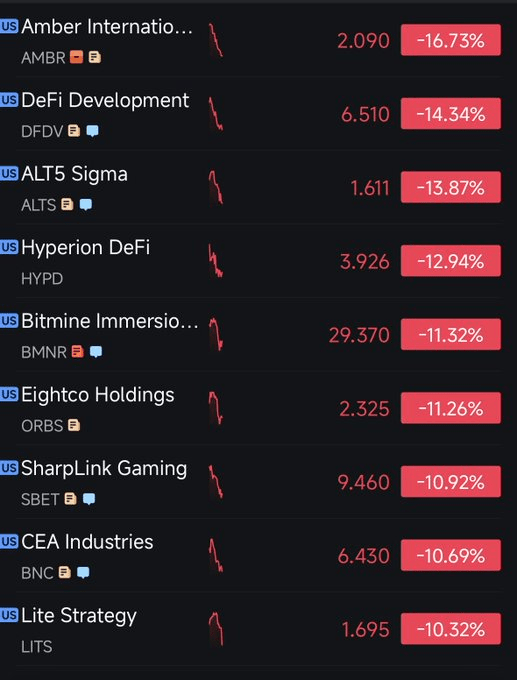

Yesterday, the U.S. stock market opened with a decline.

Stocks related to cryptocurrencies, like Bitcoin MicroStrategy MSTR and several other crypto sector stocks, have all fallen to recent lows.

This is mainly because the Bank of Japan hinted at a possible interest rate hike.

Why does the Bank of Japan's interest rate hike have such a big impact?

Because borrowing money in Japan used to be very cheap, for example, borrowing 100 million yen had almost 0 interest.

Investors would then convert the borrowed yen into dollars to buy U.S. Treasury bonds (yielding 4%, 5%), or buy stocks, gold, or Bitcoin, and finally convert the profits back into yen to repay the bank.

As long as the interest rate differential between Japan and the United States remains, profits can continue to be made. Moreover, the lower the interest rate in Japan, the greater the arbitrage space.

Research institutions estimate that the global funds using this arbitrage method may amount to $2-5 trillion, making it the largest invisible fund in the global financial system.

They believe that this free money from Japan is one of the behind-the-scenes drivers pushing up the prices of U.S. stocks, gold, and Bitcoin.

Everyone has been using Japan's low-interest loans to inflate the prices of risky assets.

However, once Japan starts raising interest rates, the borrowing costs will increase, and this arbitrage game will no longer be playable.

People will only be able to sell off high-risk assets with tears in their eyes to pay back Japan. Therefore, the market will panic in the short term.

Can the Federal Reserve's interest rate cuts offset the impact of Japan's rate hikes?

I think it can partially offset.

Because Japan's rate hikes are forced asset sales, which is ‘passive reduction’ of positions.

In contrast, the Federal Reserve's rate cuts release new hot money, which is ‘active increase’ that can prevent the money in the market from being completely drained.

As long as the Federal Reserve starts cutting rates, the new funds brought in can alleviate the outflow pressure caused by Japan's rate hikes.

Additionally, the United States officially halted ‘quantitative tightening’ on December 1, marking an important turning point, indicating the end of the ‘draining’ era that began in 2022.

By then, more funds will flow into the market, which is a long-term positive for risky assets.

How is the on-chain data?

From the Bitcoin data, this drop did cause some panic, but mainly among those who had just bottomed out in the last two days.

Those who bought around $90,000 are the ones selling the most today.

Others who bought at different price levels seem relatively stable, with no obvious signs of panic.

The restoration of confidence will have to wait for news from the Federal Reserve.

From the perspective of chip distribution, it remains stable, with no signs of a large number of losing investors selling.

Especially those whose holding costs are above $100,000 remain the largest holders and have not panicked and sold off due to price drops.

MicroStrategy MSTR has only bought 130 bitcoins this past week due to prioritizing debt repayment. They currently hold a total of 650,000 bitcoins.

At the same time, they announced the establishment of a $1.44 billion reserve fund specifically to pay dividends and debt interest to preferred stockholders.

They hope that even if there is no new income within a year or if Bitcoin prices plummet, the company can still pay interest on time without financial risks.

This is mainly because they were too aggressive when issuing preferred stock financing previously, and now they have to pay high interest to holders every year.

Currently, MicroStrategy needs to pay $750-800 million in fixed dividends each year to the shareholders who participated in the preferred stock financing earlier.

A large portion of this money was obtained by selling stocks on the market, but currently, due to poor stock performance, it is difficult to continue selling.

MicroStrategy's current CEO Phong Le stated that the company plans to consider selling Bitcoin when the stock price falls below mNAV (net asset value per share) and funding channels are exhausted.

He also clarified that this is purely a financial decision; as a Bitcoin reserve company, they are not particularly keen on selling Bitcoin, but when the market is bad, financial decisions must take precedence over personal emotions.

I believe that if MicroStrategy sells Bitcoin, it would be a good thing for them, especially when mNAV is less than 1, because it would be like an ETF.

Moreover, selling Bitcoin itself is a way to reduce leverage. In the short term, it is not good for Bitcoin, but in the long run, it is beneficial.

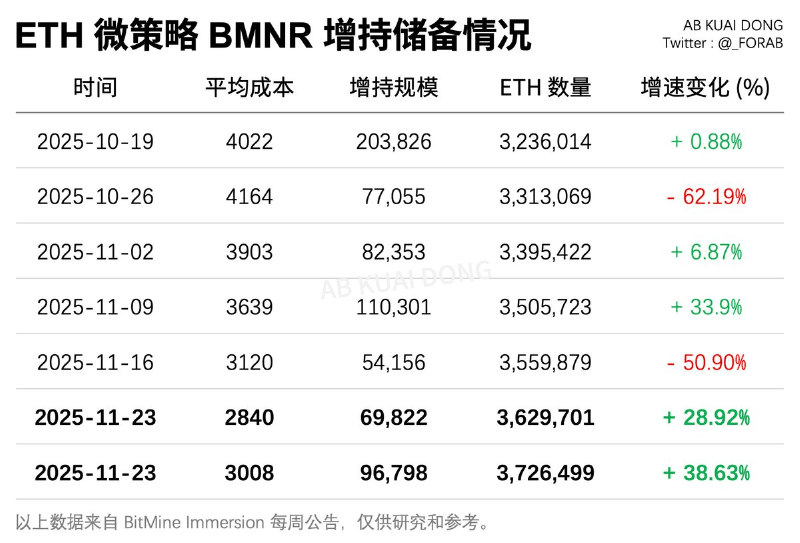

On the Ethereum side, Tom Lee's BMNR continues to buy Ethereum.

Last week, they spent $283 million to buy 96,798 Ethereum, and the amount purchased has been steadily increasing over the past two weeks.

They currently hold a total of 3.726 million Ethereum, with an average cost of $3,960, currently facing a floating loss of $4.22 billion.

They have now accumulated 3% of the total Ethereum in the network, far exceeding the Ethereum Foundation, getting closer to the 5% target.

So overall, this drop is mainly due to the market's expectation that the Bank of Japan may raise interest rates.

But we must see the essence; Japan's rate hikes are only a short-term disturbance, while the Federal Reserve's easing is the main theme of the market.

As December approaches, there will be more macro events, and in a market full of uncertainty, investors will panic, leading to increased market volatility.